Sally Beauty Holdings Inc. (SBH, Financial)Â is a cosmetics and accessories retailer serving consumers and the beauty services industry. Its focus is on selling hair color and hair care products. The company is interesting because its stock recently hit a five-year low and it has excellent free cash flow.

The latest blow to Sally Beauty was dealt by Amazon.com Inc. (AMZN, Financial) when it announced a new section on its website devoted to beauty professionals, offering stylists, barbers, hairdressers and estheticians a new alternative to their local beauty supply store. Certain beauty brands can only be purchased by licensed estheticians and hair dressers. Amazon will directly cater to this clientele.

Sally Beauty's quarterly figures for the last six years are displayed in the table below. The chart provides five series of data:

- Enterprise value.

- Market capitalization.

- Revenue.

- Operating income.

- Net income.

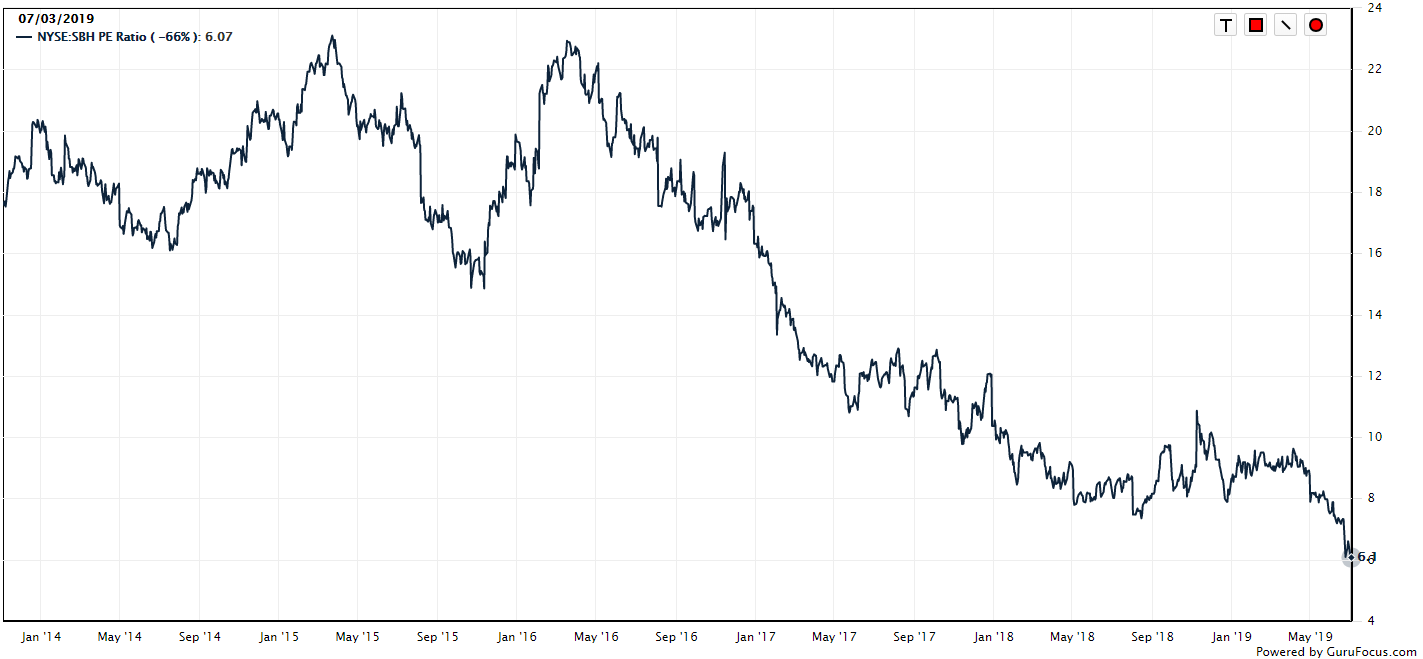

While the enterprise value and market cap have been falling over the past several years, revenue, net income and operating income have been flat. The problem is not hard to identify. Sally Beauty has been suffering from massive compression in the earnings multiple. Just take a look at the plummeting price-earnings ratio.

Investors who were willing to shell out $22 for every $1 in earnings in 2015 are barely paying $6 for the same. With a price-earnings ratio of 6, the market is indicating it expects the company's earnings to shrink 40% before stabilizing (I consider a price-earnings ratio of 10 to be appropriate for a "zero growth" company).

Taking a page out of Best Buy's playbook

With new competition from Amazon, Sally Beauty now joins the fight to stay afloat, along with many other retailers. Not all is lost, however, as Best Buy Co. Inc. (BBY, Financial), another specialty retailer that faces stiff competition, has proven it can co-exist with Amazon and do quite well.

Amazon CEO Jeff Bezos has famously said, "Your margin is my opportunity." The company started eating into Best Buy's market share by undercutting its prices. People would come into Best Buy to check out its products and then order them from the e-commerce giant. Once the retailer realized what was happening, it introduced a price matching system. This pulled the rug out from under Amazon.

Best Buy also started to focus on exclusive products so manufacturers, who had exclusive deals in place, could showcase their products. It started to leverage its physical stores as mini-warehouses so customers can order a product online, then choose whether to pick it up or have it shipped to their home at no additional cost. The retailer also started to leverage its direct relationship with customers through its Geek Squad and In-Home Advisor programs, which sends consultants to customers' homes to offer advice and help them decide if and what they would like to purchase. It is important to note the advisors are non-commission and on salary, so are under no pressure to "close the sale" and are encouraged to establish long-term working relationship with customers, similar to what pharmaceutical reps do with doctors.

The following chart shows Best Buy and Sally Beauty's performance over the last six years.

By offering its clients a complete ecosystem of know-how, best prices, curated and exclusive products, customer service and omni-channel distribution, Sally Beauty can use Best Buy's playbook to fight back.

Among the resources it has are sales consultants with its Beauty Systems Group, who service salons directly. By leveraging their knowledge and expertise and building close relationships with salon professionals, it can outmaneuver Amazon. Margins will likely shrink, but the stock will recover because even modest growth will demonstrate to the market that Sally Beauty is not dead yet and price-earnings multiples will expand. Beauty is still very much a sensory business, where products are bought and sold in experiential ways. How much Amazon is able to disrupt this business remains to be seen, but for now, I think the market has overreacted to its entry.

Investment thesis

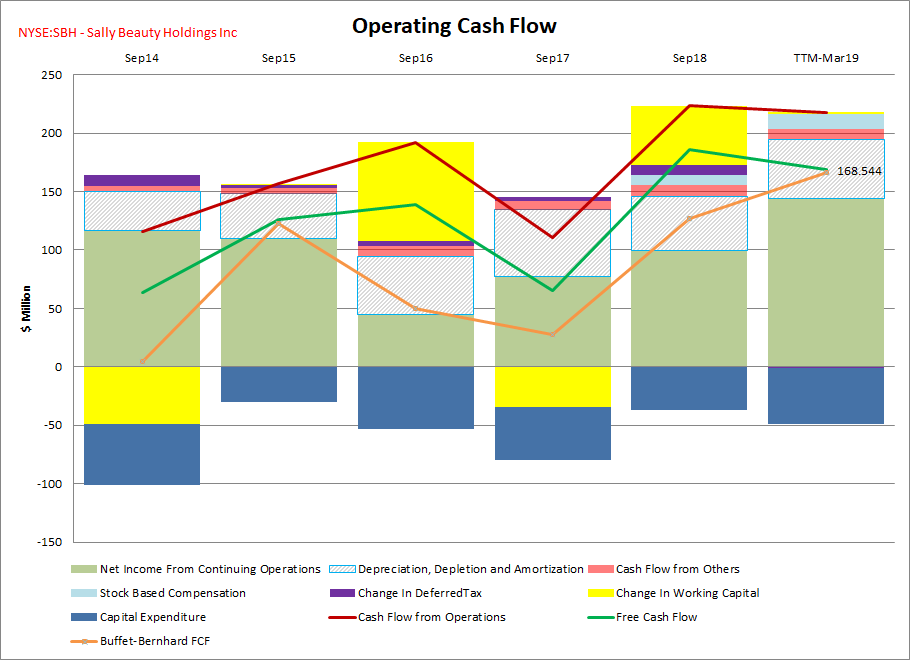

The investment thesis here is quite simple. The market has panicked and there should be regression to the mean eventually. The company is very cheap and is in no danger of going under. In 2018, it recorded adjusted free cash flow of $286.5 million ($186 million non-adjusted) and has a market cap of $1.43 billion. Sally Beauty's balance sheet is in good shape as it has $1.8 billion in long-term debt. Debt maturities occur in 2024 and 2026.

| Â | $Million |

| Term loan B (2024) | $843.1 |

| 5.500% senior notes (2024) | $200.0 |

| 5.625% senior notes (2026) | $750.0 |

| Total debt | $1,793.1 |

Source: March 2019 Investor Presentation

Management has indicated a change in strategy, focusing more on debt reduction than stock buybacks.

Chart 4: Author's calculations with data from GuruFocus.

Sally Beauty is pushing digital innovation hard. It has improved its e-commerce offering and introduced mobile apps for both iOS and Android devices. It has introduced a loyalty program, which rewards customers with $5 for every $50 spent in addition to other promotions.

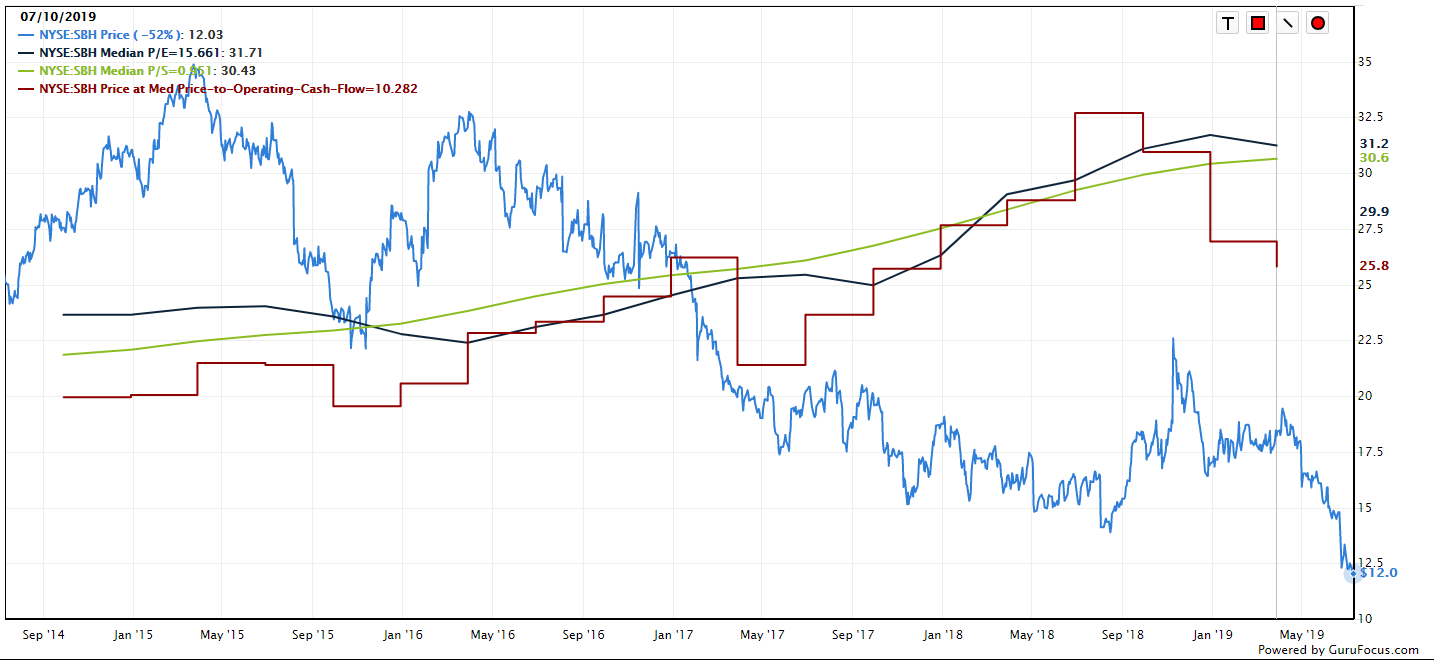

The chart below illustrates justified stock values based on median price-earnings, price-book, price-sales and price to cash flow ratios. All of them indicate the stock is very undervalued.

Morningstar continues to report a very high short ratio.

| Short % of float (June 13) | 34.67% |

When the dust settles and the Amazon scare abates, the stock price should return to the high-teens or low-$20 range. I don't think this is a buy and hold stock as, like most retailers, it does not have a moat. It is strictly a regression to the mean value play.

Disclosure: I own Sally Beauty.

Read more here:

- CRH Medical Is a Speculative Buy

- Titan Logix Is Recovering With the Canadian Oil Market

- Investor Disgust May Have Created an Opportunity in The Kraft Heinz Company

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.