The market has spoken and it wants the reinflation trade to work no matter what surfaces "in 6 months" as reality. Hence, I suppose we have to begin paying attention to the energy complex in much closer fashion - it's first half 2008 all over again. That whole Great Recession thing was just a 9 month blip I guess.

There are an avalanche of earnings this week in the oil and natural gas space - frankly, I don't know how much it matters either in this sector or most sectors. If you are in the right space you can post all the bad news in the world (see US Steel) and you will be taken up with the "rising tide lifts of all boat" trade soon enough. But I'll pretend that fundamentals matter and post some of the data points...

EOG Resources (EOG, Financial) was one of our holdings in 2008; this is a good sized ($18B market cap) exploration company that deals with both natural gas and oil, but I consider it more of a natural gas play. Unlike Chesapeake Energy (CHK, Financial) [similar size company] which reported a horrid $5.75 Billion Loss (give that CEO a raise! oh wait, he already was just granted another $100+ million after being washed out on margin calls - highest paid CEO of 2008), EOG actually did quite well. Oh yes to be fair, as long as you EXCLUDE 1x items, Chespeake did fine too; remember, 1x items don't count in analysis of American companies; even if they are $5 billion 1x items... otherwise we cannot punish management for making bad decisions. And then how would we grant them hundreds of millions in pay?

Contrast "as long as you exclude our bad decisions we rocked a profit" Chesapeake with EOG Resources. Keep in mind all these firms hedge their pricing to some degree, some well - some not so well. This was a small miss, but small misses are the new "beats" - at least if you are in blessed sectors.

Basically buying these are a 2nd derivate play directly on your "bet" on the pricing of oil and gas in the future. I used to think there was some safety in subsectors such as oil services - deep sea oil drilling specifically but if this past year has taught us anything is that differentiation in subsectors is meaningless. Wheat = natural gas = oil = corn = potash = oil services = copper. It's all just a big sector move by institutional money in and out. Deep sea oil drillers are not much different than a copper producer to these guys.

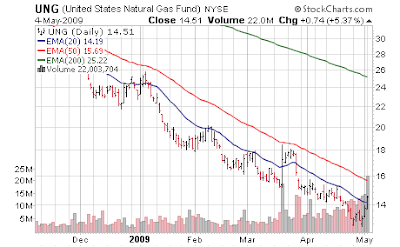

Time to reaquiant myself with Bakken, Haynesville, and Marcellus! [Jul 9, 2008: Haynesville Natural Gas Plays Refuse to Sell Off] [Jul 10, 2008: Bakken Shale Making More North Dakotans Rich - Continental Resources +20%] Natural gas is ALL the way back to prices 2 weeks ago - and we have explosion after explosion upward in stocks related to it. Have to love the logic - stock prices are far higher than they were 3 weeks ago even if the underlying commodity is the same or lower. Magic. Clearly the US recession is over as shown by natural gas spiking back to where it was in mid April - just another green shoot. It's again... all a bit bemusing; the same prices that struck no excitement 2 weeks ago now are cause for speculative fever.

[Feb 29, 2008: Natural Gas Focused Exploration & Development Companies Continue to Shine]

No positions

Trader Mark

www.fundmymutualfund.com

There are an avalanche of earnings this week in the oil and natural gas space - frankly, I don't know how much it matters either in this sector or most sectors. If you are in the right space you can post all the bad news in the world (see US Steel) and you will be taken up with the "rising tide lifts of all boat" trade soon enough. But I'll pretend that fundamentals matter and post some of the data points...

EOG Resources (EOG, Financial) was one of our holdings in 2008; this is a good sized ($18B market cap) exploration company that deals with both natural gas and oil, but I consider it more of a natural gas play. Unlike Chesapeake Energy (CHK, Financial) [similar size company] which reported a horrid $5.75 Billion Loss (give that CEO a raise! oh wait, he already was just granted another $100+ million after being washed out on margin calls - highest paid CEO of 2008), EOG actually did quite well. Oh yes to be fair, as long as you EXCLUDE 1x items, Chespeake did fine too; remember, 1x items don't count in analysis of American companies; even if they are $5 billion 1x items... otherwise we cannot punish management for making bad decisions. And then how would we grant them hundreds of millions in pay?

Chesapeake Energy reported a huge first-quarter loss Monday on write-downs in the value of its natural gas and oil properties, falling short of Wall Street's bottom-line forecasts by a narrow margin. The company announced that it lost $5.75 billion, or $9.63 a share, in the most recent quarter, compared with a loss of $142 million, or 29 cents a share, a year ago. Revenue rose 24% to just under $2 billion from $1.61 billion a year ago. Here comes the magicExcluding items, the company said it had adjusted net income of $277 million, or 46 cents a share. Analysts were expecting 48 cents on an EPS basis. Too bad we can't all be judging our net worth and profitability once we exclude the bad things. So you know what to do on the 6% drop in after hours - buy Chesapeake hand over fist immediately. Myself, I have them in permanent Hall of Shame so I'd rather deal with EOG or XTO Energy (XTO) or Apache (APA). In many ways these are not based so much on earnings; the story is really their portfolios and the ebb and flow of prices.

Contrast "as long as you exclude our bad decisions we rocked a profit" Chesapeake with EOG Resources. Keep in mind all these firms hedge their pricing to some degree, some well - some not so well. This was a small miss, but small misses are the new "beats" - at least if you are in blessed sectors.

Oil and gas exploration company EOG Resources Inc. said on Monday that its first-quarter profit fell 34 percent. The company said it earned $158.7 million, or 63 cents per share, during the quarter that ended March 31, down from $240.5 million, or 96 cents per share, during the year-earlier period. Revenue rose 2 percent to $1.16 billion, from $1.13 billion a year earlier.The company said it had mark-to-market hedging gains of $226.1 million after taxes, or 90 cents per share. If those gains were counted in the quarter in which the hedge settles, EOG said it would have had a first-quarter profit of 53 cents per share. Analysts surveyed by Thomson Reuters were expecting a profit of 59 cents per share on revenue of $976.9 million. The company said it was raising its full-year 2009 organic production growth target from 3 percent to 5.5 percent. It said domestic crude oil and natural gas liquids volumes were running stronger than expected. Chairman and CEO Mark G. Papa said the company is optimistic that crude prices will strengthen later in 2009 and that natural gas prices will recover in 2010.I am surprised they are still expanding production to such a degree myself, but they seem to be able to make money, with the hedges at least.

Basically buying these are a 2nd derivate play directly on your "bet" on the pricing of oil and gas in the future. I used to think there was some safety in subsectors such as oil services - deep sea oil drilling specifically but if this past year has taught us anything is that differentiation in subsectors is meaningless. Wheat = natural gas = oil = corn = potash = oil services = copper. It's all just a big sector move by institutional money in and out. Deep sea oil drillers are not much different than a copper producer to these guys.

Time to reaquiant myself with Bakken, Haynesville, and Marcellus! [Jul 9, 2008: Haynesville Natural Gas Plays Refuse to Sell Off] [Jul 10, 2008: Bakken Shale Making More North Dakotans Rich - Continental Resources +20%] Natural gas is ALL the way back to prices 2 weeks ago - and we have explosion after explosion upward in stocks related to it. Have to love the logic - stock prices are far higher than they were 3 weeks ago even if the underlying commodity is the same or lower. Magic. Clearly the US recession is over as shown by natural gas spiking back to where it was in mid April - just another green shoot. It's again... all a bit bemusing; the same prices that struck no excitement 2 weeks ago now are cause for speculative fever.

[Feb 29, 2008: Natural Gas Focused Exploration & Development Companies Continue to Shine]

No positions

Trader Mark

www.fundmymutualfund.com