The 92-year-old entertainment major, The Walt Disney Company (DIS, Financial), has steadily grown in size and scale over the years, while overall revenues have been growing at above 4% range since the great recession. Their revenue growth has continued well into this year, as Walt Disney posted a solid 9% sales growth in the first nine months of this year compared to last year, while net income expanded by 13%. But the market seems to remain unimpressed as Disney’s stock is down 8.76% since the start of the year. The company is currently trading at a low 16.5 times earnings.

Let us take a closer look at Walt Disney’s numbers to understand why the market believes that the company deserves such a low valuation.

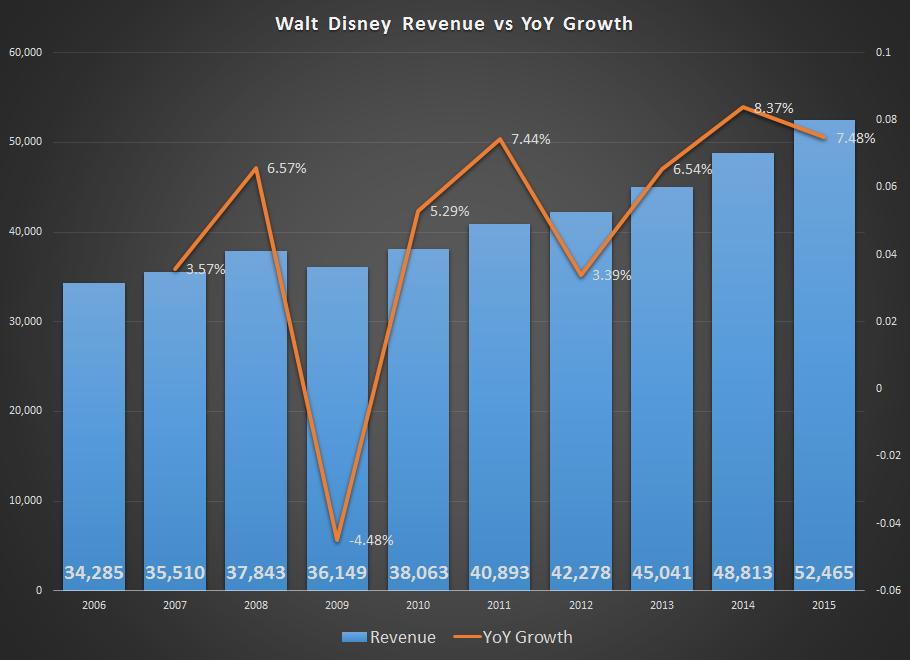

Disney is a Boring Company!

The biggest problem Disney faces is that it has been around for way too long. Despite stable growth for so many decades, Disney’s business lines - media, parks and resorts, studio businesses and consumer products - do not seem to excite people any more, investors included. So instead of rewarding the company for growth, they have come to expect it as a given. That is a reasonable assumption considering that news from Disney is not treated the same way as news from Facebook (FB, Financial) or Google (GOOGL, Financial).

That’s the psychology behind the market’s attitude towards Disney as a company, but what are the numbers? Does Disney deserve its current low valuation or are investors being unreasonable?

Disney by the Numbers

With 44% of their 2015 revenue coming from Disney’s media networks, which includes marquee brands such as ESPN, the Disney Channel and ABC news, they operate in a highly penetrated and highly competitive market.

These are stable revenue streams that will post safe growth at best of times and drop a bit at the worst. Revenue growth will never be spectacular, and buying more properties will be the best short at revenue expansion.

In 2014, Media network segment’s revenue grew by 4%. In 2015, it grew 10% and in the first nine months of the current fiscal, it has grown 3%. It has largely stayed on the positive side and with nearly half of their revenues coming in from this segment, Disney’s overall performance obviously depends on this segment very heavily.

One of the biggest disappointments for Disney investors is that their lead brand, ESPN, reported a decline in the number of subscribers.

“Data from Nielsen released last month showed ESPN subscribers declining at a rate of about 4% over the previous year versus a rate of about 2% last year. But the data don’t take into account streaming services.”

- WSJ

With subscriber growth stumbling and the only growth opportunities seeming to come from contractual rate increases to affiliates and ad unit growth, it is understandable for the market to be pessimistic about the growth runway ahead of the company.

In their Q3- Earnings Call, the company said:

“At cable, we saw nice operating income growth at ESPN, driven by higher affiliate and advertising revenue. Growth in affiliate revenue at ESPN resulted from increases in contractual rates, partially offset by a decline in subscribers and unfavorable impact from foreign exchange. ESPN ad revenue was up 5% in the third quarter, driven by an increase in units sold.”

With subscriber growth stumbling and the only growth opportunities seeming to come from contractual rate increases to affiliates and ad unit growth, it is understandable for the market to be pessimistic about the growth runway ahead of the company.

A New Opportunity in Media

With the traditional Pay-TV model on the decline as streaming over the internet grows, media empires are in a state of transition. Disney is transitioning as well, but there are two bits of good news around that.

First, this is not going to happen overnight. Second, even if their traditional market share and numbers start to dwindle faster than expected, Disney is well positioned to capture market share in video streaming. The company is already part of a consortium that owns popular video streaming site Hulu LLC and is steadily investing in that segment. During the third quarter earnings call, the company also announced that it has acquired a 33% stake in BAM Tech, a digital video distribution and analytics platform, and would be launching a direct-to-consumer subscription streaming service for live sporting events with ESPN branding.

It’s clear that Disney’s growth via ESPN may not be as strong as before due to the change the industry is going through, but Disney is one of very few companies this size that are ready to embrace the new delivery model.

At the current price point, trading at 16.5 times earnings, Disney’s stock looks very cheap for the kind of assets it has under its belt.

Disclosure:Â I have no positions in any stocks mentioned and no plans to initiate any positions within the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.