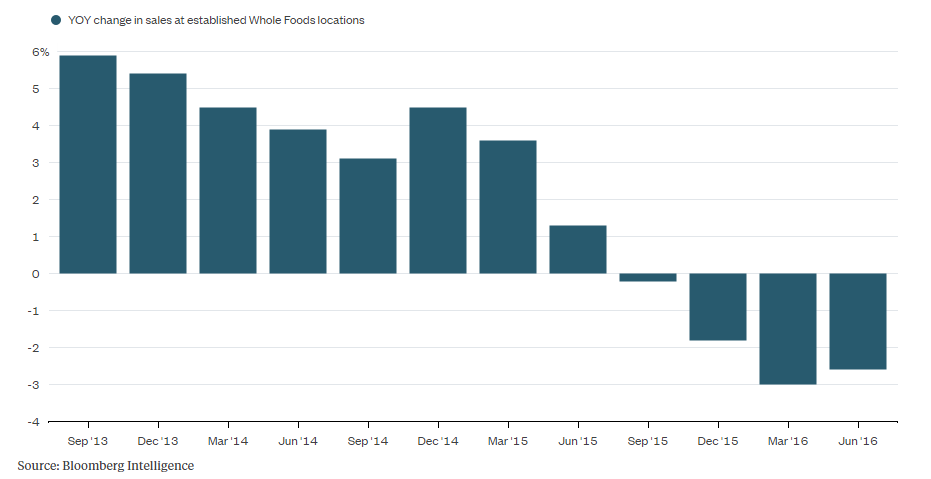

Grocery giant Whole Foods’ (WFM, Financial) fortunes have swung in the opposite direction with respect to comparable store sales, which have been declining for four straight quarters. After staying above the fold during the 2013-2015 period, comps went negative during fourth quarter of the last fiscal, a trend the company is yet to break. The stock has been trading in a tight range of $28 to $34 since October 2015, as if the market is still unsure of what to do with the company.

To be fair, Whole Foods nearly tripled its revenues in the last ten years, going from $5.6 billion in 2006 to $15.3 billion in 2015. It is only in the last four quarters that the company has been showing some weakness, which can be attributed to rising competition from all directions. As Amazon (AMZN, Financial) turned up the pressure on big box retailers, companies such as Wal-Mart (WMT, Financial) and Kroger (KR, Financial) have intensified their focus on groceries, which is their biggest earner.

Target Corporation (TGT, Financial) is another prime example. The company faces severe headwinds on the sales front, but has finally realized that grocery is an important segment that needs extra attention. During the most recent earnings call, Target CEO Brian Cornell said:

“While our grocery business was negatively impacted by food deflation, which accounted for about 20 basis points of pressure, we clearly have more work to do to unlock the growth potential in this important category. Given our recent performance and the increasingly competitive food environment, we are revisiting our second half grocery efforts from presentation to assortment to promotion to improve our competitive position.”

The Price Point Disadvantage

One of the key reasons for Whole Foods’ growth in the past was the way the company differentiated itself from others. Their products have always been more expensive, for example.

“We compared the prices of 31 items at a Whole Foods store in Glen Allen, Virginia to an identical set of items at a nearby Kroger store.

The Whole Foods basket was about $60 more expensive than the total at Kroger.”

But people were agreeable to paying higher prices because they were searching for higher quality and healthier products, and that is exactly where Whole Foods positioned themselves. As Whole Foods started searching for more sales, however, it made the mistake of bringing its prices down to attract more customers, and the company started a new chain called 365 to offer lower-priced products.

Although the jury is still out on the recent initiative, the branding of the parent chain is bound to get hurt. With lower prices, 365 will obviously need a larger footprint and more traffic to compensate for losses at Whole Foods’ larger stores. On the other hand, if they open too many stores, it could eat into the earnings of their core brand.

The company panicked at the first smell of competition and, while offering the same type of goods at two different price points sounds good on paper, the overall effect is not going to go over well with loyal Whole Foods customers - and that is exactly what the company is going through right now, sagging sales for the last four quarters.

The better route would have been to stand its ground and focus on brand marketing and other initiatives that would have justified higher prices. Instead, they chose to take the bait offered to them by the competition, and are now paying for it. The company not only sent a mixed message to its customers, but eroded their own brand value in the process.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.