Travelers Companies (NYSE:TRV) is the third-largest provider of property and casualty insurance and one of the best managed. In this report, we'll be outlining why Travelers combines an extremely attractive valuation with strong price momentum, solid profitability and shareholder-friendly management. We'll also outline how Travelers has been crushing analyst estimates recently and is poised to continue doing so. Before we begin our analysis, investors should know a little about our analytical style. Our analysis focuses on identifying and exploiting stock market "anomalies." We've identified a variety of different academically tested metrics that have a long track record (over 50 years) of predicting stock returns. We'll provide links to the academic papers that fuel our analysis as we progress through the report so you can see for yourself whether to trust the metrics we rely on. Click here to see a detailed breakdown of the prominent academics (many of whom manage billions of dollars) and their contributions to the field of stock research that we draw inspiration from.

Valuation breakdown

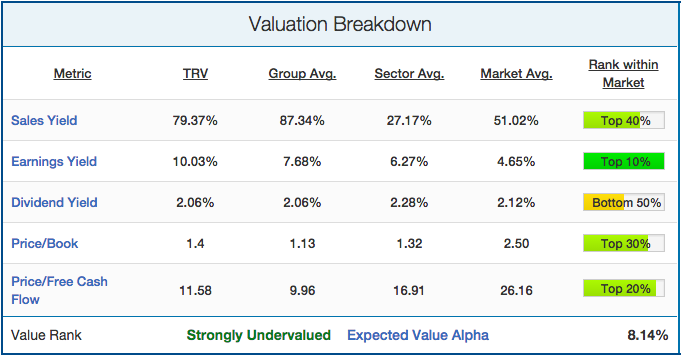

We'll start with an analysis of Travelers' valuation profile, looking at five valuation metrics each with a strong predictive ability. This is important to consider as Nobel laureate Eugene Fama showed that "value stocks have higher average returns than growth stocks." The "value" anomaly is the strongest and most consistent edge in the market, as study after study has shown that cheap stocks beat expensive stocks. TRV's valuation profile is shown below:

(click to enlarge) Source

Source

Like the broader insurance industry group, Travelers looks significantly undervalued relative to the overall market on almost every measure of value. On a earnings basis, Travelers' earnings yield of 10.03% is more than double the average stock in the market (4.65%) and significantly higher than both the insurance industry group (7.68%) and financial sectors (6.27%) averages. Travelers trades at 11.58x free cash flow, which is less than double the free cash flow multiple of the average stock in the market (26.16x). Stock looks attractive on a revenue and book value basis as well, with a sales yield (79.4%) and price/book multiple (1.4) both significantly more attractive than similar rates for the average stock in the market. Travelers has a solid dividend yield of 2.06%, though as we'll detail later, the company is primarily returning capital to shareholders through aggressive buybacks. Overall, our models rates Travelers as "Strongly Undervalued" relative to the market and expects the stock to generate significant ex-ante alpha moving forward as this undervaluation is priced in.

Growth breakdown

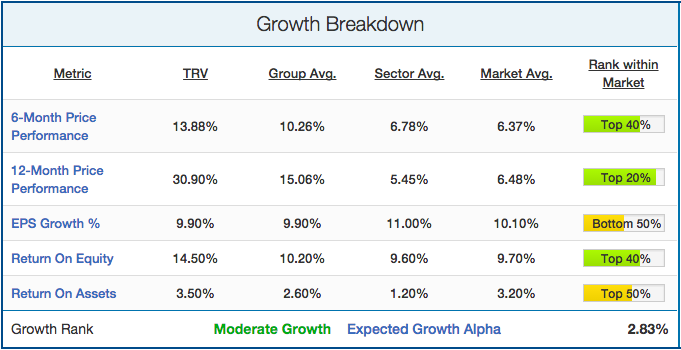

There is a variety of different growth metrics that have been shown to predict stock returns. Most important among them is price momentum. Winning stocks keep winning (based on six-month price performance), and losing stocks keep losing. As outlined in James O'Shaughnessy's book What Works on Wall Street, EPS growth and return on equity/assets also were shown to have predictive ability, albeit to a lesser extent. TRV's growth breakdown is shown below:

(click to enlarge) Source

Source

Travelers' stock price gained over 31% the last 12 months, more than double the average insurance stock (15.1%) and more than quadruple the performance of the average financial stock (5.45%). The stock has also outperformed over the last six months as well, gaining 14% versus a gain of 6.37% for the average stock in the market. This is a key differentiator between Travelers and other insurance stocks. While Travelers is not the most undervalued stock within the industry, the market has begun to pick up on its potential. This type of recognition from the market, which manifests in strong price performance, is crucial to good future investment performance. Travelers' profitability growth is solid with TTM EPS increasing 9.9%, which is largely the same as the industry group, sector, and overall market averages. Profitability is efficient, with Travelers returning 15% on equity versus 10% for the average insurance stock. Overall, our models rate Travelers as a "moderate growth" stock and expect its growth profile to contribute to significant outperformance for the stock over the market over the next twelve months.

Upcoming earnings breakdown

Next, we'll see how TRV has been performing relative to analyst expectations recently. We've found through historical back testing that stocks that have a history of beating analyst expectations are much more likely to beat estimates in the future. We've used this earnings model to predict earnings ahead of time on the crowd-sourced earnings platform, Estimate. Using this model on over 500 quarterly earnings estimates, we've attained a very high analyst confidence score of 8.3/10. This is key as stocks that beat analyst estimates often see big jumps in price, thus it is crucial to have an idea of how earnings will come out ahead of time. TRV's earnings breakdown is shown below:

(click to enlarge) Source

Source

Travelers crushed last quarter's EPS consensus number by 21%, which was the ninth time in the last ten quarters that the company beat analyst estimates. The company also beat consensus revenue estimates, which was its eighth time to do so in ten quarters. Clearly, Travelers has a history of beating expectations and surprising to the upside. This is key as companies that have a history of beating estimates are far more likely to keep beating in the future. Travelers releases next quarter's earnings in 25 days, with analysts polled by Zack's forecasting $2.60 EPS and $6.64 billion in sales. Our models expect them to crush EPS estimates by a wide margin (>7.5%), and to beat revenue estimates by a solid amount (2.5-7.5%). We rate this company as a pre-earnings "buy," meaning that investors would do well to increase their position prior to the earnings release.

Qualitative analysis and conclusions

Now that we've analyzed the numbers, it is essential to have a qualitative discussion of potential growth catalysts and business risks. The most important catalyst behind Travelers' stock is the company's aggressive share repurchase plan. As estimated in a recent Seeking Alpha article, Travelers has about $1.5 billion left in their current share repurchase plan. This amounts to over 4% of Travelers' total market cap. Buybacks drive up share prices by not only increasing demand for stock but also by driving up EPS through the removal of shares. Additionally, buybacks limit downside in the stock, as you can be sure that company management will be sure to employ share repurchases if Travelers sees any big negative moves in its stock price.

Many on Wall Street are predicting that Janet Yellen will begin the process of monetary normalization with an increase in interest rates at the FOMC meeting in September. On an overall macro basis, this will be a headwind to stocks by raising the costs of capital and likely fueling a further increase in the dollar. This will be true for most companies, as they tend to "debtor" companies that owe more debt than they own. On the other hand, for those few "creditor" companies that own more debt than they owe, interest rate normalization will be a significant tailwind. This is especially so for insurance companies, which generate a large portion of their revenue from the investment returns of the massive cash float they sit on. For this reason, along with systemic undervaluation and overall strong growth profiles, we have written extensively on the benefits of buying into insurance companies right now (see MetLife). Travelers has an unrealized gain of $2.67 billion in fixed income securities, which would get whittled down if interest rates were to rise. With that being said, over the long run, higher interest rates would allow Travelers to generate a higher yield on their cash float.

Overall, Travelers combines an attractive valuation with strong price momentum, a track record of crushing analyst earnings estimates and future industry tailwinds. We rate the stock as a "strong outperform" and expect its returns over the next 12 months to significantly beat the returns of the S&P 500.