I hate to invest in large caps. It's my belief a dollar buys a lot more in the nano cap store. I'll keep shopping there as long as I can. Google (GOOG) (GOOGL) is one of only three large caps in my portfolio which is diversified across ~50 holdings. For me to venture into large cap territory, I must really like the investment. I do love Google at the $547 level. So much so that Google is my largest position.

The hard part of my thesis is explaining why Google is so incredibly undervalued while hundreds of analysts worldwide follow the company and publish research on it. Literally everyone who has ever bought a share knows the company. The media is all over Google and its crazy ventures and reports on every little thing the company comes up with. Why then, does the market not get that there is virtually no downside and tremendous upside at its current ridiculously low price?

It's human nature to have a hard time differentiating between the signal and the noise. There is so much information on Google that people slowly lose sight of what drives Google's value and what doesn't. There is a lot of press about the self-driving cars, Project Loon, elevators into space that make great headlines. It's all incredibly fun stuff to debate, discuss and mock, but ultimately none of it makes much of a difference to the bottom line except for blowing up CapEx, but more about that later.

Something very close to 90% of Google's revenue comes in through Google sites and Google Network Member sites. Google shows ads on its own sites (like Google.com) and shows ads on network member sites and gets paid by the advertiser or gets paid by the advertiser and shares revenue with the member site or content partner (like on YouTube). Pretty much everything else is noise.

First lets look at Google's core business and its sustainability. Specifically, Google's search engine and Google Adwords engine.

Google search

Google is absolutely dominating search with a market share of 60% worldwide. The next largest competitor only has a 10% market share. I´ll briefly go into why market share is so important.

Search quality becomes much better if you have extensive knowledge of the searcher. This is one of the reasons people often name Facebook (FB) as a possible challenger to Google. Sure Facebook also has extensive knowledge of you, enough to serve you solid contextual ads. However, the most important thing to know about someone to improve the quality of his or hers search results is his or her search history. Google is collecting the valuable search history on 60% of all search users. With every search switching costs become higher for its users and Google's service to them becomes better. If you don't immediately grasp how valuable your search history is, think of how helpful it is to know that someone studied at NYU and compare that to when presented with 10 links on previous searches for "NBA tonight" knowing which links he or she ended up selecting. Which data is most helpful the next time this person is pulling up data on upcoming NBA matches?

Because Google is collecting the absolute most important context to provide a good search experience; search history on 60% of all human beings with access to an internet connection (while making the conscious choice to stay out of China). It will be extremely hard to match the quality of search Google provides by a new incumbent.

The longer this status quo lasts, the harder it will be to pry market share away from Google. In my opinion, its competitive advantage is incredibly robust.

Initially Google's competitive advantage was derived from its superior technology but even when Google is surpassed by the superior technology, that is sure to emerge, it will be very hard to overcome the data handicap.

Google ad engine

The Adwords/Adsense ad engine is really interesting. With Adwords you can, as an advertiser, bid on keywords to have your ads shown when users search for that keyword. Paying more helps you to rank higher, but Google also assigns your ad a quality score. The more useful your ad is to the searcher, the less you need to pay in order to rank high. This is the reason why we aren't flooded with insurance and banking commercials. If you have a website, you can sign up to Adsense, and your website is included in Google's inventory of ad space. You give up a revenue percentage to Google as opposed to selling the ad space yourself, this saves A) lots of time and effort in selling space B) Google has a huge inventory of advertisers and knowledge of the person that visits your site, enabling it to serve highly relevant ads resulting in more clicks and thus money for you and Google.

I'm still surprised how efficient Adsense is in monetizing a web property. Even major websites like GuruFocus elects to rely on it, although it obviously has the scale and reach to sell its ad space on its own. An advertising network has a competitive advantage when it reaches a certain critical mass because it becomes more interesting to both advertisers and customers with each new connection. With how much information Google has on its users and its current scale, I think its safe to say the ad network has a huge competitive advantage.

Strategic review

Google could do just fine for a long time by just exploiting its major assets as best it can. Major shareholders and key executives Page, Brin and Schmidt don't think that's the best strategy.

To understand the strategic rationale that governs Google's decisions, it helps a lot to read the founders letters, freely available from its website and How Google Works and In the Plex are also tremendously helpful books to learn more about the search giant.

At Google there is a great hunger to leverage its core technology of search and its ad engine into a company with a much greater reach. Management takes an exceptional approach to find the best ways to do this, which is exemplified by the famous and often derided Moon shots, which the company describes as follows in its annual report:

The idea of trying new things is reflected in some of our new, ambitious projects. Everything might not fit into a neat little box. We believe that is exactly how to stay relevant. Many companies get comfortable doing what they have always done, making a few incremental changes. This incrementalism leads to irrelevance over time, especially in technology, where change tends to be revolutionary, not evolutionary. People thought we were crazy when we acquired YouTube and Android, and when we launched Chrome. But as those efforts have matured into major platforms for digital video and mobile devices, and a safer, popular browser, respectively, we continue to look towards the future and continue to invest for the long-term.

We won't become complacent, relying solely on small tweaks as the years wear on. As we said in the 2004 Founders' IPO Letter, we will not shy away from high-risk, high-reward projects because we believe they are the key to our long-term success. We won't stop asking "What if?" and then working hard to find the answer.

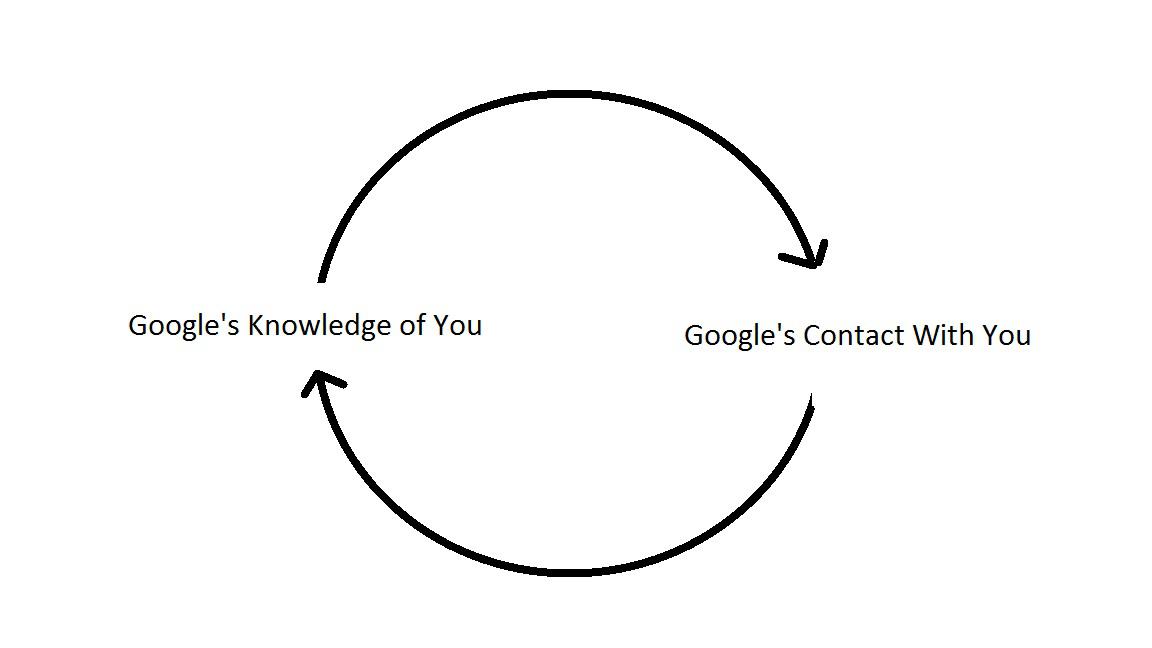

At first I wasn't too happy with the moon shots. Like many investors all I could see was Google loading up the cannon with cash, firing and hitting %&@(. The way I now look at Google the moon shots and other investments make sense (as all over the place as they are). Think of Google's strategy like this:

(click to enlarge)

Source: Author's own

The company's strategy is to increase its knowledge of you and its contact with you. It is critical to the company that it keeps this virtuous cycle going. Note how the company often chooses user experience over profit. Google wants to avoid breaking the cycle at all cost. It will find a way to monetize you somewhere along the way but it's very careful this doesn't break down the cycle.

When you view Google's investments and moon shots within this broad strategic framework (including successes like Android and YouTube) they tend to make sense.

Risks

Google has a rock solid competitive advantage. In the 2008 crash, it didn't even take a breather, cash kept coming in. Google is optimized to gain the trust of its users, its deliberately not squeezing its users for all it can in the short term. Not only do I think there is sound theory behind this, it means the company is much more robust than it appears.

Although it has virtually no debt, if it came to a situation where it needs every penny it can get, it has options. A very different situation from a company that has tapped every cash flow opportunity and then gets in rough water.

Strangely enough, the internet was initially unlocked through portals, such as Yahoo! (YHOO), Geocities, etc. That didn't cut it and search took over. Now there is another flavor of curation with apps. Ultimately to find the right app at the right time I think search technology and knowledge of the user will be invaluable. I'm fairly certain Google will find its role in the Appverse.

There are many challengers to Google's business of being in contact with you. One competitor that is often highlighted is Facebook. Truth is, there are countless media that capture the attention of customers and that have the scale to attract advertisers and exploit their content themselves without using Google's ad services. No one is effectively challenging Google in its primary role of providing you with exactly the right answer at the right time. Facebook is limited to showing you answers derived from within its user generated content, but Google unlocks all the information on the entire web, and having intimate knowledge of your search history will make its solutions stronger.

Investors often express concern about Google's founders involvement with the company and their disregard for Wall Street, short term profits and love of Moon Shots. There is even a Captain of Moon Shots at Google. I used to have these concerns myself. With the founders holding a lot of voting shares, there are no guarantees they will not engage in shareholder value destructive behavior. However, what greatly mitigated my concern was reading the founders' letters and "How Google Works" by Eric Schmidt. I've come to appreciate the company's long term view. I support how it builds up an ever greater competitive advantage. It does so by placing customers first and generating trust which allows the company to collect information to make its products ever better.

The media jumps all over the latest Google Moon shot and admittedly, some can appear to be pretty far out there. If you view Google's strategy as increasing contact with you and knowing more about you, everything falls into place. It takes them to weird places but Google is trying to build relationships with everyone on this planet.

This costs money, but building up the relationship first and maintain it for some time is hugely helpful to build a competitive advantage. It's expensive, but try to pry a customer away from Google. It's even more expensive, Microsoft (MSFT) will tell you.

Regulation is not so much a threat in the U.S. but it is a bit of a concern in Europe. I think this is for the most part a short term threat. Regulators are particularly interested what Google is doing with its users data. It is exactly that data collection that is also key to a great search experience. Limiting data collection or not allowing Google to use it will hamper search. Hampering search (access to information) is probably a good way to hurt your economy. Not in a direct way but by significant opportunity costs. With its "Don't be evil" mantra and its investments in lobbying, it should be able to convince regulators to make rational decisions. Even if regulators decide to act more strongly against Google, they may change their minds confronted with the results.

Catalysts

With the company in its current state there are a few major events that could wake the market up and unlock value that is immediately apparent:

Repatriation tax lifted

There are rumors that U.S. companies could be presented with a repatriation tax windows where they could bring home cash and be taxed at a lower rate. With some $30 billion "trapped" overseas, a window like that may incite the company to bring some home and disburse it to shareholders. Management alluded it certainly would enter the equation as far as capital allocation goes if this were to happen.

High CapEx innovation

Critics have no trouble coming up with ways to ridicule Google's Moon shots that would require major CapEx to realize if turns out to be actually feasible. There is an upside to that, too. Remember how Buffett is suddenly in love with these businesses requiring tremendous amounts of capital; railroads and utilities in particular. These investments allow him to take the tremendous Free Cash Flow Berkshire Hathaway's (BRK.A) (BRK.B) subsidiaries produce and funnel it in a tax efficient way into additional cash producing assets.

Google's core capital light monopoly like business is brilliant but a decent high CapEx requiring business would be a great opportunity to drive shareholder value at a greater than average rate. Especially if the overseas cash hoard could be utilized this way. If this venture would be synergistic with Google's core strategy of increasing knowledge of- and Google's contact with you, that opportunity it could easily be a huge winner.

Europe closing the gap in ad spending

From personal experience, I can tell you that many small and medium businesses in the Netherlands are under utilizing Adsense. I hear this all the time when I meet small and medium business owners, but it's also reflected in Google's relatively modest revenues from Europe. U.S. and Global revenue has been pretty balanced near 50:50 for quite some time. Europe is a much larger economic block than the U.S., but Google's revenue is lagging big time. In the short term this will be exacerbated by the FX. Obviously, global GDP growth is going to be a major driver for the company over the years, but I think Europe can make a big difference in the short term (1-3 years).

My entire story boils down to that the market is making Google's valuation too complicated. Google's market value is correct if you assume its current CapEx is required to sustain its existing business, and this business continues growing at the somewhat slower rate it has over the past five years. It's also correct if you put some value on Google's Moon shots and other ventures, but expect its core business growth to slow down significantly.

If you take current EBITDA which is around $21.5 billion and estimate the company requires a $1.5 billion in maintenance CapEx. That means it's trading at a TEV/Ebitda - maintenance CapEx ratio of just ~15x.

Considering its wide moat and good growth prospects (given the widely documented Global GDP growth and Global growth of internet consumption). In my view, the easiest way to see Google's value is to realize you are effectively getting everything outside of the core business for free. Including (but not limited to):

(click to enlarge)

Prius modified to be a driverless car, not having to drive you will be connected more often, patents will be valuable to license. Source: Wikipedia.

Dropcam bought for $555 million, to monitor your home remotely, Source: Nest store

Nest bought for $3 Billion+, Source: Nest store

Motorola patent portfolio bought for $12.5 billion, Mobile division has been resold to Lenovo, source: Gadgets.ndtv

(click to enlarge)

Waze, traffic App bought for close to $1 billion, Source: Thefusejoplin.com

(click to enlarge)

Google Loon project, will balloons provide internet access on planes, remote areas and poor areas. Source: Wikipedia

(click to enlarge)

Airborne wind power technology, source: Makani website

(click to enlarge)

Well publicized Google Glass venture, connected at all times. Source: Dogtown media

(click to enlarge)

App advertising and discovery company Red Hot Labs, source: Red Hot Labs

How much are these bonuses worth to you? I'm convinced there is not a lot of downside to Google at its current price. What its exact upside looks like is extremely uncertain. My thesis is, you are getting that upside, from the Moon shots and growth surprises, pretty much for free. At the same time, there is very little risk Google will not continue to be able to generate boat loads of cash. In fact, it can increases cash flow signficantly if pressured. That's why I decided to load up even though Google is a large cap stock. I'm not alone in my belief Google is undervalued because such esteemed value investors like Mohnish Pabrai (Trades, Portfolio), David Tepper (Trades, Portfolio), William von Mueffling, Christopher Davis, David Winters (Trades, Portfolio), William Fries, David Rolfe (Trades, Portfolio), Wallace Weitz (Trades, Portfolio), Harry Burn, Steven Romick (Trades, Portfolio), Thomas Gayner, Thomas Russo and Bill Nygren (Trades, Portfolio) hold stakes in the company. I think that's pretty good company to be in.