Archer Daniels Midland (NYSE:ADM) has been a major beneficiary of low corn and energy prices, as well increased demand for ethanol. ADM is the largest producer of ethanol in the United States, with 25% of the production market share. The collapse in crude oil has hurt ethanol producers even though the ethanol price has stabilized, and oil is an input price (therefore a decline in oil is a good thing). Additionally, because the collapse in oil has spurred demand in gasoline (due to cheaper prices), ethanol demand should actually grow. ADM is a diversified company that actually generates the majority of its revenues from food products (such as soybeans, soybean meal, etc.)

In this report, we'll be outlining why investors should use the recent correction in ADM's stock price to open up or increase their current long positions. Based on traditional value metrics that have been empirically shown to predict stock returns, ADM is strongly undervalued relative to the market. Additionally, ADM has a solid growth profile and the "smart money" is moderately bullish on the stock. Again, the metrics used to highlight this have been empirically shown to predict returns, and are thus are extremely important to analyze. As we go through the report, we'll provide links to the academic papers that underpin our analysis so investors can see themselves why each metric is important. Investors looking to dig deeper into academic research, can check out our post, which outlines the major academics and their research.

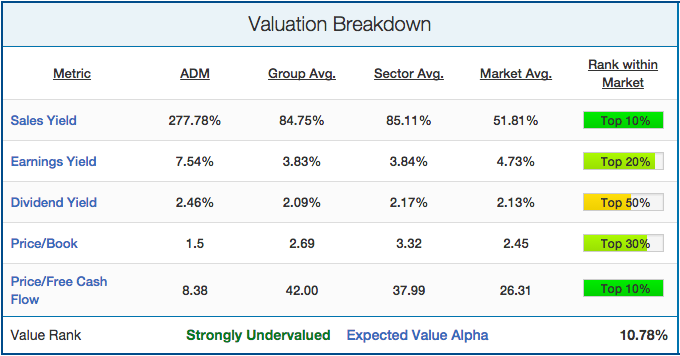

Valuation breakdown

We'll start with an analysis of ADM's valuation profile, looking at five valuation metrics each with a strong predictive ability. This is important to look at as Nobel Laureate Eugene Fama showed that "value stocks have higher average returns than growth stocks." ADM's valuation profile is shown below:

(click to enlarge) Source

Source

On every metric shown above, Archer Daniels Midland looks relatively undervalued. ADM has a sales yield of 278%, based off trailing 12-month revenue of $81.2 billion and a market cap of about $29 billion. That means investors can currently get $2.78 of sales for every $1 they invest in the company, which is more than triple the average for stocks in the Food Products industry group. ADM is much more reasonably priced on an earnings basis with its earnings yield of 7.5%. Again, this is almost double the industry group average (3.83%), though it is only moderately better than the overall market average (4.73%).

ADM's massive undervaluation is most pronounced on a free cash flow basis. Trading at a multiple of 8.4x free cash flow is borderline insane when comparable Food Product stocks trade at 42x and the overall market trades at 26x free cash flow. Yes, there are worries about the future prospects of ethanol. But with the EIA forecasting increased ethanol production in 2015 & 2016 and with the company in little danger of bankruptcy any time soon, this move is wildly overdone. Additionally, ADM pays out a solid dividend yield of 2.5% that isn't expected to be cut any time soon. Lastly, trading at a multiple of 1.5x book value ensures limited downside should anything dramatic happen. Overall, based off these metrics our algorithms rate ADM as "Strongly Undervalued" and expect the stock to see significant outperformance over the S&P 500 in the next twelve months because of this.

Growth breakdown

There is a variety of different growth metrics that have been shown to predict stock returns. Most important among them is price momentum. Winning stocks keep winning (based on six-month price performance), and losing stocks keep losing. As outlined in James O'Shaughnessy's book "What Works on Wall Street," EPS growth and return on equity/assets were also shown to have predictive ability, albeit to a lesser extent. Archer Daniel Midland's growth breakdown is shown below:

(click to enlarge) Source

Source

While ADM's stock price has nosedived the last six months (-9%), the stock is still up 10% on the year. This is much better than fellow ethanol producers Green Plains Renewable Energy (NASDAQ:GPRE) and Pacific Ethanol (NASDAQ:PEIX), both of which are down more than 35% in the last six months. This reflects ADM's diversity in operations, as the company derives the majority of its revenues from food products such as soybeans (16% of sales), soybean meal (13%) and corn (10%).

Sales have slightly declined over the last four quarters in part due to ADM selling previously unprofitable businesses (such as its chocolate, cocoa and fertilizer segments). This hasn't hurt the bottom line, though, as ADM has grown EPS by 70% on a trailing 12-month basis. This is more than six times the Food Products industry group (11%) and overall market (10%). Besides shedding underperforming businesses, management has proven its efficacy with solid return on equity and asset rates (11.2% & 5.4%). Overall, our algorithms rate ADM as "Slight Growth" company, implying mild outperformance over the S&P 500 because of its growth.

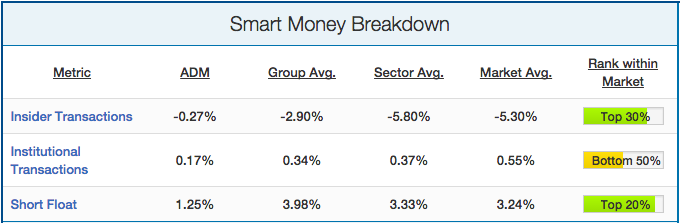

"Smart money" breakdown

In addition to value and momentum, we will also analyze how the "smart money" on the street is playing ADM. "Smart money" stakeholders are short sellers, company insiders and institutions. Each of these stakeholders tends to be much more sophisticated than the average investor. We have found loads of academic research showing that short sellers, company insiders and institutions all predict stock returns. This breakdown is shown below:

(click to enlarge)

There are a few things to glean from the table above. First, ADM company insiders have essentially maintained their positions in stock while company insiders in the industry group (-2.9%) and overall market (-5.3%) have been significantly decreasing their positions on average. Company insiders tend to know their business and its true valuation better than everyone else so it's very telling that ADM insiders haven't followed suit with insiders across the market in selling. Institutions have mostly maintained their positions in ADM, reflecting a broad trend across the market. Short sellers have been very optimistic on the stock, with short interest representing only 1.25% of the entire float. This is actually very unusual for a stock that has decreased by 10% over the last few months, as short interest tends to increase during stock price declines. It's a very good sign that short interest in the stock is less than half the industry group average, even when the price performance has severely lagged the group. This emphasizes our overall thesis that investors should use this dip in price to increase their long exposure to the stock. Overall, we rate the "Smart Money" as moderately bullish on the stock, with positive implications for the price over the next twelve months.

Qualitative analysis and conclusions

Now that we've run through the numbers, we'll begin a qualitative discussion of potential growth catalysts and business risks facing ADM today. As announced in the February earnings call, management is increasing its share buybacks to $1.5-$2.0 billion over the next year. At a market cap of $29 billion, this represents over 5% of the total float. This once again reflects company management's competency, as management is smart enough to realize that its stock is significantly undervalued and is thus using the opportunity to return capital to shareholders. It will also increase buying pressure during any major corrections, as company management will utilize their buybacks during any major declines in stock price as a form of price support. Share buybacks have been shown to predict stocks returns, especially when the stock is undervalued. Overall, we are extremely bullish on Archer Daniels Midland over the next 12 months. We rate it is a "Strong Outperform" due to its severe undervaluation, solid growth profile, and the bullish sentiment of the "smart money" on the street.