What You Will Learn

- Why I purchased CRUS in the first place

- Why I don’t hold stocks like CRUS over a long period

- A deeper look at the 4 warning signs that make CRUS a sell today.

After a 60% gain, it’s time to sell Cirrus Logic (CRUS, Financial)

For this to make sense, I need to explain why I purchased CRUS in the first place.

I found the idea from the Forbes best small companies list. I actually get a lot of ideas from here every year because it fits a lot of my criteria and a lot of the work is already done for you.

Most of the companies on this list are fairly easy to understand too. CRUS was a simple idea that didn’t need a detailed 20 page due diligence report for me to make an investment.

Here’s where I started buying CRUS.

Starting Buying CRUS | Enlarge

It’s just luck that I bought towards the bottom. I usually go in with the belief that the stock is going to fall more after I buy, but it wasn’t really the case this time.

That’s partly why I also didn’t have a huge position. It would be awesome to say that I had strong conviction and bought a big position, but that wasn’t the case.

Now anyone that knows CRUS understands that the company is entirely dependent on Apple (AAPL) as a customer with > 80% of revenues coming from Apple.

There’s always chatter that CRUS is going to lose its socket place in Apple devices.

Pricing power and threat of competition is continually discussed.

The truth is that Cirrus Logic is never going to be a long term hold type of company. There are far too many real risks that have been covered.

But every company can become an opportunity at the right price.

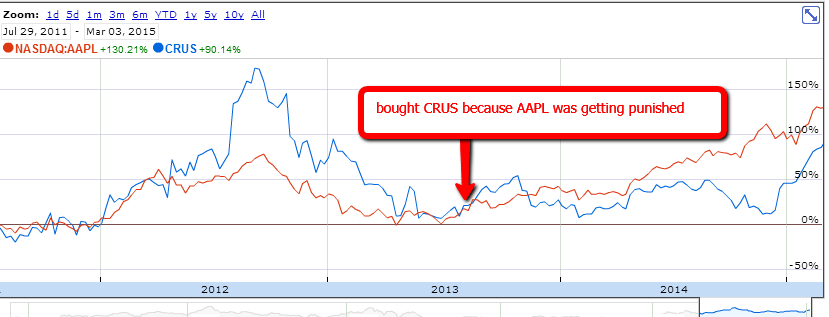

Why I Bought CRUS in the First Place

My idea was to use CRUS like a form of “leverage” with my Apple position. Instead of using options or doubling down on Appl, I purchased CRUS on the reasoning that

- people were expecting a definite socket loss position based on a teardown of the iPad Air

- uncertainty and fear was overblown

- if the sentiment towards Apple turned, then Cirrus Logic was going to benefit from it

And as luck would have it, all three points turned out in my favor and the following happened.

As Apple gained favor again, CRUS rose Apple wave back up.

In hindsight, the smarter move was to just double down on Apple. The profit would have been higher and I wouldn’t be faced with what to do after selling CRUS. I would just be happily holding to AAPL for years to come.

CRUS and AAPL Moving Together | Enlarge

Now you know I love my valuation exercises.

I do it for every company I come across, and although CRUS still generates a large amount of cash, the current price no longer puts it into attractive territory.

My estimates using DCF, EPS and other various valuation models that I use with my stock analyzer, gives me an intrinsic value range between $30 and $36.

Good Luck Until Now. Takes Skill to Make the Decision to Sell When Things Change.

If CRUS had a clear competitive advantage, it’d be easy to label it as a hold.

Below $20 a share, the negativity about the over dependence on Apple and loss of pricing power is an opportunity.

But at $30 and above, it’s no longer an opportunity. It’s a risk.

Warning Signs with Cirrus Logic

Here are some other numbers that make it risky for me at this point.

- An EV/EBIT multiple of 17x which is the close to what it was trading for in 2012, and 2012 has better numbers.

- Decreasing margins does indeed indicate a lack of pricing power. Gross margins in the mid 50% is history now. The TTM gross margin is 47% and continues trending down. The latest quarter has margins at 44% compared to 47.4% in the comparable prior quarter.

- Drastic drop in performance metrics indicating difficulties. See the image below.

Bad Signs Brewing | Enlarge

The large drops across the board in TTM ROE, ROA, ROIC and CROIC are definitely worrisome.

With short term stock prices moving based on guidance and estimates as opposed to fundamentals, this is an indication to me as a value investor to sell out while the market is still happy.

Look deeper at how and why ROE has been dropping using the DuPont analysis and you’ll see some warning signs.

5 Step DuPont Analysis is Awesome for Quality Checks | Enlarge

If you look at the numbers above, the three issues that pop up is the fall in operating margins, drop in asset turnover and increase in leverage.

Those three factors caused ROE to drop to 6.5% in the TTM.

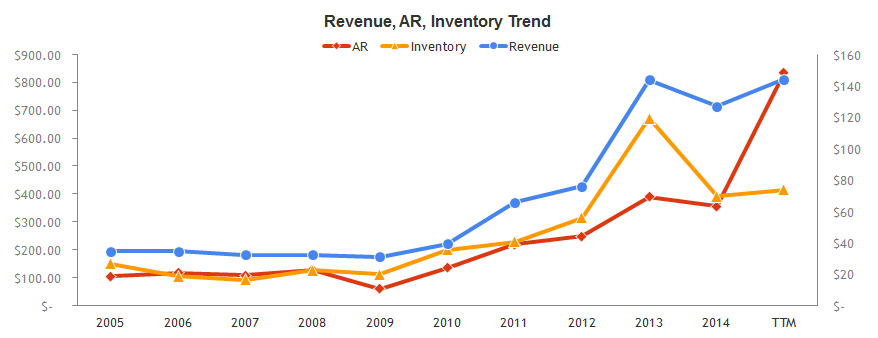

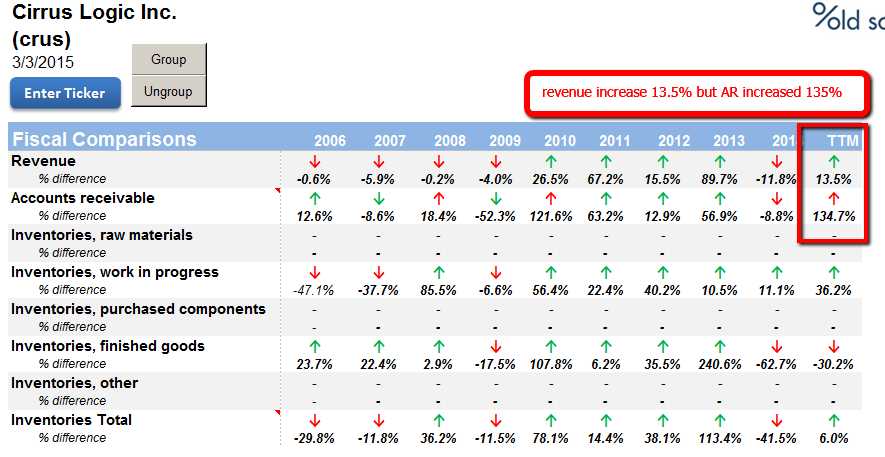

Another quality check that I consider a very good indicator of future performance is the correlation between revenues, accounts receivables and inventory.

Red Flag with Receivables

I’m seeing a big red flag in this chart.

Accounts receivables ballooned and increased faster than revenue. It’s been continually rising the past 3 quarters.

The ideal scenario is for all three lines to be parallel with each other. That would make for a perfectly managed company.

However, accounts receivables shooting up like this means that it’s being squeezed by customers or being too lenient with their terms to get business.

Big Disconnect Between Revenue and Receives | Enlarge

Either way, it’s a bad sign when revenue only increased 13.5% but accounts receivables is up 135%.

I previously lost a lot of money from a company where receivables shot through the roof. The situation was different to CRUS because the company at the time was in financial distress and they ended up pushing their product onto store shelves without understanding the consequence of inventory bloat and not collecting inventory.

So I take it seriously when accounts receivables shoots up 120% more than revenue.

Get Access to More Stock Ideas

Get instant access to our ideas via email. We'll send you stock analysis spreadsheets as a bonus.

4 Reasons that CRUS is a Sell Today

- EV/EBIT is too high

- Declining margins

- Huge drops in performance ratios

- Red flags with receivables

None of these warning signs were there 1 year ago. But at $30 a share and signs of deterioration, it’s time to liquidate CRUS, lock in a 60% gain and move on.

CRUS is not a hold simply because it has no competitive advantage and any downturn for a company like CRUS will see that the stock price is hammered.

My intrinsic value range estimate was $30 to $36 and although it’s not at the peak of the range, I’m more than happy to move on.

I’ll call this one lucky.

But isn’t luck also a skill?

Disclosure

Selling CRUS