MetLife (NYSE:MET), the largest U.S. life insurer, announced a 68% profit increase for Q1 2015 on February 11. Since then its share price has remained relatively stagnant ($1 increase). MET continues to trade at 80 cents on the dollar despite being a growing, undervalued company. The reason for this is regulatory uncertainty, the recent SIFI (systemically important financial institution) designation and fear of low yield curves becoming the norm. We believe these fears are overblown and that MET is a buy because it is extremely undervalued, there is institutional confidence in the company, and the recent uptrends in yields have already started to pump the stock up. For investors willing to wait for interest rates to come up (and they will eventually), MET is a clear buy. We'll start this article with a quantitative breakdown of the company's relative value, then analyze its growth profile, followed by an analysis on how the "smart money" is playing the stock, before concluding with some qualitative analysis and conclusions.

Valuation breakdown

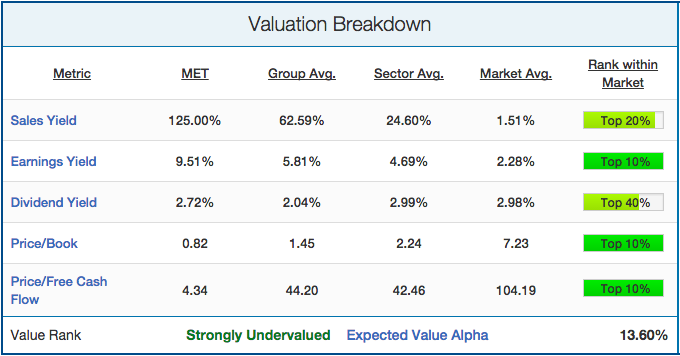

We take a quantitative approach to investing, preferring to focus our analysis on a certain set of metrics that have a strong predictive ability. We'll start by analyzing MetLife's value profile. This is important to look at as Nobel laureate Eugene Fama showed that "Value stocks (with low ratios of price-to-book value) have higher average returns than growth stocks (high price-to-book ratios)." MET's valuation profile is shown below:

(click to enlarge)

On every important measure of value, MET is attractively priced. Its sales yield (TTM Revenue / Market Cap) at 125% is essentially twice the average for the insurance group (62.6%), and nearly five times the financials sector average (24.6%). It also means that an investor can currently get $1.25 of revenue for every $1.00 they invest in a company that makes money and is rapidly growing (EPS growth of 172% this year). This type of value is very hard to find in a profitable and growing company, especially in an otherwise expensive market.

MetLife's earnings yield of 9.51% places it in the 91st percentile of the market, the 86th percentile of the financials sector and the 69th percentile of the insurance group. Its price-to-book ratio of 0.82 implies that you can buy the stock at a near 20% discount on book value, providing plenty of downside protection should anything drastic happen. Not only that, but by the end of 2014, MetLife reported a near 17% year-over-year growth in total book value per share –Â reflecting the opportunity to invest in a company that is growing aggressively.

Where MET becomes even more attractive is when its price-to-free-cash-flow ratio is considered. At 4.34, MET has a more attractive price-to-free-cash than 97% of the market, and the fifth-best P/FCF of all large cap ($10B - $100B) stocks. The company's relatively average dividend yield (1.02%) is the lone weak spot, though we believe the company should be bought for capital appreciation rather than income generation. Given these five valuation metrics, we rate MET as strongly undervalued and expect it to generate significant outperformance (13.6%) over the market due to it.

Growth breakdown

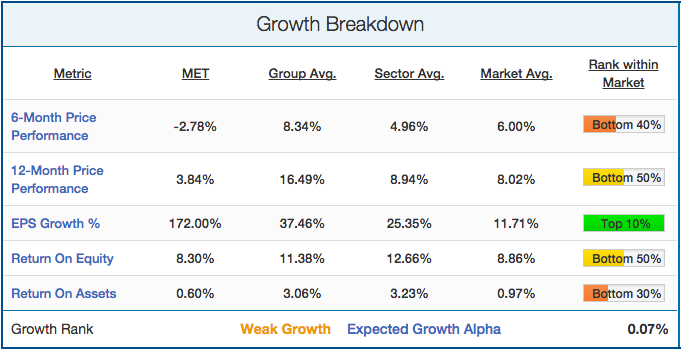

There are a number of different growth metrics that have been academically proven to predict stock returns. Most important among them is price momentum. Winning stocks keep winning, and losing stocks tend to keep losing. While we believe MET should be bought because of its value, one should never ignore metrics that have been proven to have predictive ability. MET's growth profile is shown below:

Although MET's 6-month and 12-month price performance has been relatively weak, investors have reason to be optimistic as MET's price has risen 10% in less than a month since the uptick in the 10-year treasury yield that started on Feb. 2, 2015. Though MET is relatively weak by traditional measures of momentum, the short-term activity in treasury yields should prove hopeful for investors. As we touched on above, its earnings growth of 172% is fantastic relative to any segment of the market. Finally, while ROE and ROA remain low, they have also both seen dramatic increases in the past year. Overall, we rate MetLife as a weak growth company and predict its growth metrics to have a negligible effect on driving its stock price.

"Smart money" breakdown

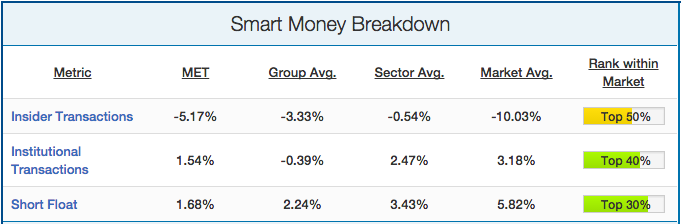

In addition to value and momentum, we will also analyze how the "smart money" on the Street is playing MetLife. "Smart money" stakeholders are short sellers, company insiders and institutions. Each of these stakeholders tends to be much more sophisticated than the average investor due to their inherent advantages. Company insiders know their company inside out while institutions and short sellers spend millions of dollars on research. We have found loads of academic research showing that short sellers, company insiders and institutions all predict stock returns. MetLife's "smart money" breakdown is shown below:

Though none of these metrics provide any definitive answers on MET, the relatively low short float and moderate institutional buying are definite positive signs. A negative insider transaction number (implying that insider ownership is decreasing) is usually a red flag; however, when compared with the market average of -10.03%, MetLife's -5.17% change in insider ownership appears to be less concerning. Overall, we rate the "smart money" as being moderately bullish on the stock, which is a good sign for the stock's future performance.

Qualitative analysis and conclusions

It's clear from these metrics that MetLife is greatly undervalued, and the reason is most likely due to regulatory uncertainty surrounding the company and industry in the past couple of years. One such concern is the SIFI designation that MetLife received on December 18, 2014 by the Financial Stability Oversight Council. Though it's not exactly clear as to what extent this designation will affect MetLife internally, the consensus is that it will limit MetLife's ability to dish out dividends as capital has to be tied up in reserves. MetLife is fighting the designation in court, though it's unclear what the outcome will be. More importantly though, low yield curves and low interest rates are the main reasons for MetLife's undervaluation. While obviously hard to predict, it's clear that interest rates will be coming up sooner rather than later (with the consensus predicting next September). Given the company's confidence in its $1B increase to its share repurchasing program, the growth in institutional purchasing, and most importantly, it's undervaluation, now is a good time to bet on MetLife in the next year. Investors looking to learn more about our analysis can do so here.