A) Introduction

Western Digital Corporation (WDC, Financial) is the dominant HDD manufacturer in the United States with more than 45% of the entire market. While HDD's are neither as fast nor durable as SSDs, they are more than seven times cheaper. So while it's true that SSDs are taking market share, HDDs are not going anywhere anytime soon. In fact, HDD sales are expected to continue to grow for the next four years (more on that later).

In this article, we'll outline why Western Digital offers the perfect combination of value, price momentum, profit growth, and efficiency. The report will start with a breakdown of Western Digital's valuation profile, then will proceed to an analysis of the price and profit growth, followed by an analysis of recent "smart money" transactions, and concluding with some qualitative analysis and conclusions. We take a quantitative approach to investing, preferring to focus our analysis on metrics that have strong predictive ability. Thus, we tend to analyze academic papers and perform historical back tests on different metrics before including them in our analysis. We will provide links to the academic papers we draw inspiration from as we progress through our breakdown of the stock so investors can see for themselves what we base our conclusions on. Investors looking to learn more about our analytical style can check out our website.

B) Valuation Breakdown

We'll start by analyzing Western Digital's value profile. This is important to look at as Nobel laureate Eugene Fame has found that "Value stocks have higher average returns than growth stocks." Western Digital's valuation profile is shown below:

(click to enlarge) Source

Source

There are a few interesting things to note from the table above. First, Western Digital is a cash flow machine. The companies free cash flow yield - which we can derive by inverting price/free cash flow - is 8.25%. This is higher than their earnings yield (6.07%) meaning the company generates more free cash flow than actual earnings. Free cash flow is a much more indicative and practical measure of how a company is performing, as it is much harder to manipulate. The fact that WDC is trading at a Price/FCF of 12 when the overall market is trading at an average of 86 shows that stock is severely undervalued on a relative basis. This is a good sign as study after study shows that stocks trading on lower price multiples tend to outperform the market. WDC looks fairly attractive on a book value basis as well, with its price/book (2.75) being lower than the industry group (3.50), sector (5.08), and overall market (6.89) averages. Overall, we rate Western Digital as "Undervalued" and expect the stock to outperform the market by 3.67% over the next 12 months.

C) Growth Breakdown

There are a variety of different growth metrics that have been shown to predict stock returns. Most important among them is price momentum. Winning stocks keep winning, and losing stocks tend to keep losing. Western Digital's growth profile is shown below:

(click to enlarge)Source

WDC has managed to overcome weakness from the computer and peripherals group over the last six months (-4.43%), gaining 6.57% versus 4.48% for the technology sector and 0.34% for the overall market. WDC was even stronger over the last twelve months, gaining 21.5% versus 3.5% for the Technology sector and 2.5% for the overall market. WDC leads the industry in profit growth (annual EPS growth of 68%), which is much higher than the industry group (-41%), technology sector (3.7%), and overall market (17.3%) averages. This is also a much better growth rate compared to its main HDD rival - Seagate Technology (NASDAQ:STX) - that had annual EPS growth of -6%. The company is also relative efficient, returning 18% on equity and 10% on assets. Once again, these stats are much better than the industry group, sector, and overall market averages. Overall, Western Digital is a "Moderate Growth" company and we expect the stock to generate 2.94% of alpha attributable to growth, over the next twelve months.

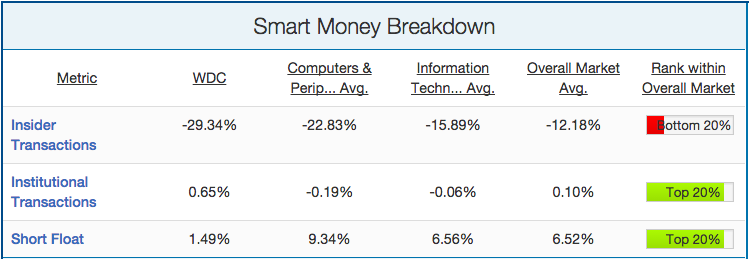

D) "Smart Money" Breakdown

In addition to value and momentum, we will also analyze how the "smart money" on the street is playing Western Digital. We consider the "Smart money" to be short sellers, company insiders, and institutions. Each of these stakeholders tends to be much more sophisticated than the average investor and thus their transactions give good clues of what is to come. We have found loads of academic research showing that short sellers,company insiders, and institutions all predict stock returns. This "smart money" breakdown for WDC is shown below:

(click to enlarge)

Looking at the table above, it seems that company insiders have been dumping the stock over the last six months (-29% in ownership). While this is disheartening at a first glance, a further look into the individual company insider transactions reveals two things. First, the majority of the insider selling comes on the same day that those same insiders execute options. This is natural and mimics the pattern seen in other companies as insiders will execute options and sell them for instant cash. Secondly, this pattern of insider selling has been consistent for the last 10 months. While this could be a worrying sign that company insiders have been dumping the stock for the last year, you could also interpret this as evidence that the recent company insider selling isn't anything to be worried about. If company insiders were selling western digital when the stock was below $86, and its now at $106 after hitting a high at $114, then their transactions haven't been very indicative of future performance.

We should note that the academic study cited above showed that company insider buying was much more predictive than company insider selling, as insiders will often sell based on non-market related motivations (liquidity, personal reasons, etc.). Additionally, company insider transactions were less indicative for large cap stocks, which WDC most certainly is ($25 billion market cap). Thus, while we are cautious about the company insider selling, we feel the extremely low short interest (1.5% of float versus 6.5% for the market) is more indicative of the future performance of the stock. The stock has also seen moderate accumulation from institutions recently (+1% in last three months).

E) Qualitative Analysis & Conclusions

We'll now supplement our quantitative analysis with a qualitative discussion of some of the major growth catalysts and risk factors that could impact the stock price in the near future. As we mentioned at the start of the article, the faster and more durable SSD's are expected to capture significant market share within the space. With that being said, the overall market pie is growing as HDD shipments are expected to grow 2.9% a year from 2013 to 2018, as indicated by Gartner research. Gartner has also believes that SSD's will "complement, not replace" HDDs as the future capacity of firms is expected to be enormous. Given that Western Digital owns 45% of the entire HDD market, they are in a prime position to capture this growth. Nevertheless, there still remains a possibility that SDDs progress faster than people expect and become cost competitive with HDDs sooner rather than later. We are firm believers in the former case rather than the latter, but nevertheless it remains a possibility.

Overall, we feel that WDC is attractive valued with strong price momentum, EPS growth, and profit efficiency. The company releases earnings Tuesday after hours, with analysts expecting $2.10 EPS (according to Zacks). Western Digital has beaten consensus estimates 11 times in a row, and thus an earnings beat on Tuesday looks highly likely. Wall Street seems to agree with our bullishness, with the average price target on the stock set at $118.32 (+12% from current price), as shown below:

We are using the recent pullback in stock price from $114 as our entry point, and expect the stock to continue its outperformance in 2015.