Urban Outfitters (URBN, Financial) might consider changing its name to Anthropologie. I was surprised that sometimes small changes like changing the corporation's name to the most profitable of its brands can help to improve the perception of a company. A good example is Fifth & Pacific, which changed its name to Kate Spade (KATE). In fact, as my pendulum analysis implies, as the pendulum swings too far to the pessimistic side, there is a good chance that patient investors can gain a good return when the pendulum swings back to the optimistic side. After today's decline, I believe that too much bad news have been reflected in the current share price. In the bullish scenario, URBN can return back to $48, implying more than 50% upside potential.

Company Overview

Urban Outfitters is a specialty retailer and wholesaler. It has three major brands: Urban Outfitters, Anthropologie and Free People. It also has some developing brands such as Terrain and BHLDN.

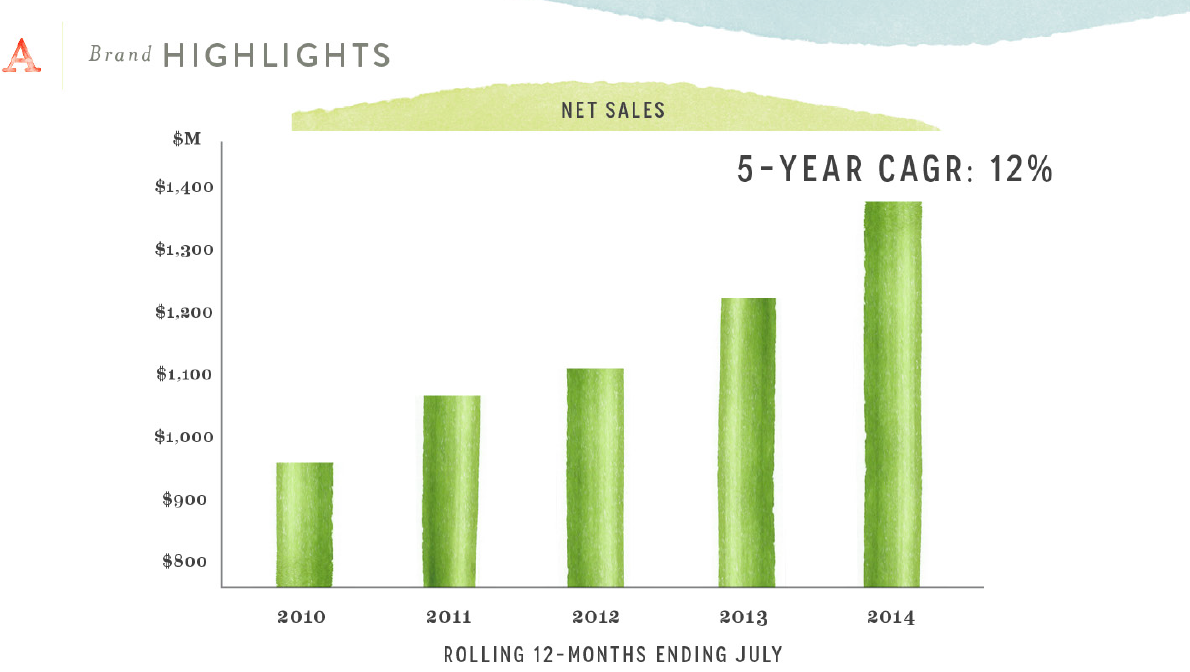

Out of the three core brands, I would like to further discuss Anthropologie. Its net sales has grown 12% CAGR since 2010.

(click to enlarge)

Source: Company Presentation

The following lists the accomplishments of the Anthropologie brand:

(click to enlarge)

Source: Company Presentation

As URBN derives 41% of total sales from Anthropologie, 44% from namesake brand Urban Outfitters, and 13% from Free People, investors should notice that both Anthropologie and Free People are still growing. With the new store opening opportunities still available for both Anthropologie and Free People, URBN will have top line growth. As the management of URBN has already realized, improvement in Urban Outfitters is the first priority.Â

A vision in 2020

URBN outlined its goal to double its revenues by 2020 while remaining one of the most profitable companies in the sector. Its strategy is to expand offerings, enhance the customer experience, and grow distribution.

Why did URBN decline?

In last month's conference call, the management team did not seem to give any hint of further negative comparable sales in Q3. Nevertheless, in less than one month, URBN provided a negative update as follows:

Urban Outfitters, Inc. ("URBN') announced today that third quarter negative comparable retail segment net sales, as reported in its Form 10-Q filed in earlySeptember 2014, has continued quarter-to-date. Due to the lower than expected sales, URBN believes its gross profit margin may deleverage for the third quarter at a rate greater than during the first half of the year. If this were to occur, the Company's third quarter earnings would be negatively impacted.

In today's volatile stock market, investors have already been very nervous about negative news. Plus, the surprise negative announcement above damages the credibility of the management team to navigate the current brutal retail environment. As a result, URBN declined by approximately 13% before the market open today.

For long-term investor, we should check our intrinsic value of URBN and see whether we will get a good deal in investing in URBN or not. This leads to my valuation section below for my fellow readers.

Valuation

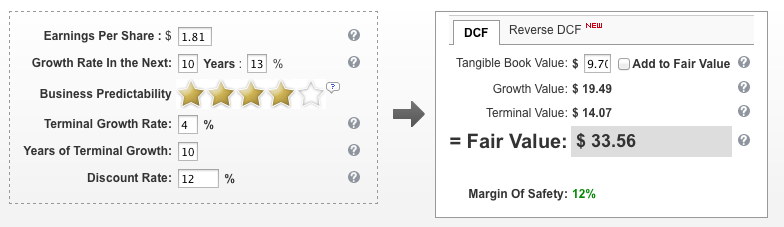

(click to enlarge)

Source: Gurufocus.com

First and foremost, URBN scored very well with the DCF model generated by Gurufocus.com. There is 12% margin of safety. Plus, URBN scored 4 stars out of 5 in terms of business predictability.

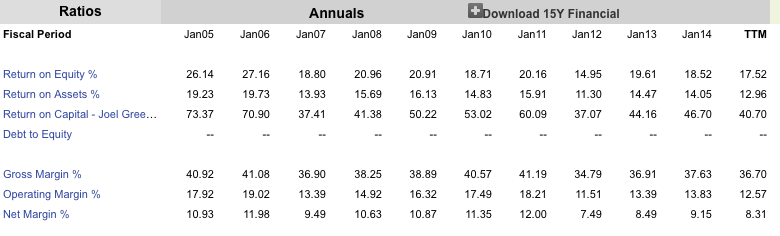

(click to enlarge)

Source: Gurufocus.com

As we can see, the lowest net margin of URBN is approximately 7.5%. As we all know about the issues with Urban Outfitters, I further assume that there is not much growth from the $3 billion sales in 2014. I still came up with a low estimated net profit earning capability of $230 million.

Given the current enterprise value of about $3.6 billion, URBN is currently trading slightly below 16x enterprise value over earning ratio. In my opinion, the current valuation of URBN is low relative to the potential of what URBN can achieve. In addition, there are not many retailers capable of obtaining at least 7.5% net margins. That's one of the reasons why URBN used to command a premium valuation relative to its peers.

To see how conservative the current valuation I assigned for URBN, we can see the following excerpt from Barron's:

AT NEARLY $37 A SHARE, Urban Outfitters trades at 17 times 2015 projected earnings, an enticing discount to the 20 times forward earnings it typically fetches.

Jaffe sees the stock rising to $48 a share, or just under 22 times his 2015 estimate of $2.24 a share, representing a possible gain of about 30%

If URBN can increase its profit margins and reverse the same store sales decline in the Urban Outfitters brand, the $2.24 EPS should be within reach.

What retail investors should do is to buy companies, like URBN, when the expectation is low instead of high. Another critical point investing in URBN is about business fundamental. URBN has always been the king of e-commerce, which most retailers must be admired for the online commerce achievement of URBN. Indeed, URBN is the leader with more than 25% of total sales coming from e-commerce. Plus, other than the trouble with Urban Outfitters, both the Anthropologie and Free People have been performing well. The following is the excerpt from the latest Q2 2015 earning announcement:

Comparable Retail segment net sales at Free People and Anthropologie Group increased 21% and 6%, respectively

Investors should independently think about what is the fundamental behind URBN. Is the current low expectation in favor of accumulating URBN? I believe that the fundamental of URBN does not change so rapidly in the year, but the expectation does. Personally, I would rather buy retailers when their expectation is low rather than high so as to capture the potential return once the expectation drives higher in the future. Nevertheless, there is one cautious note. We should first strive to find companies with strong fundamental and then wait for investment opportunities to come like what has just happened today for URBN.

Positive Outlook

URBN has significant presence in the mobile and social network. Its Free People brand was ranked the first as below:

(click to enlarge) Source: Company Presentation

Source: Company Presentation

In addition, URBN mainly focuses on the United States currently. It can actively pursue international expansion opportunities. As URBN becomes a more global retailer, I believe that it can leverage its brands and generate higher profit margins in the international market.

Share Repurchase Program

During the second quarter of fiscal 2015, the Board of Directors authorized the repurchase of 10 million common shares under a share repurchase program. During the second quarter of fiscal 2015, the Company repurchased and retired 3.7 million common shares for approximately $126 million, leaving 6.3 million shares available for repurchase under the current authorization.

Not only does URBN have $409 million cash, cash equivalents and marketable securities, but also URBN has good financial discipline to return capital back to shareholders.

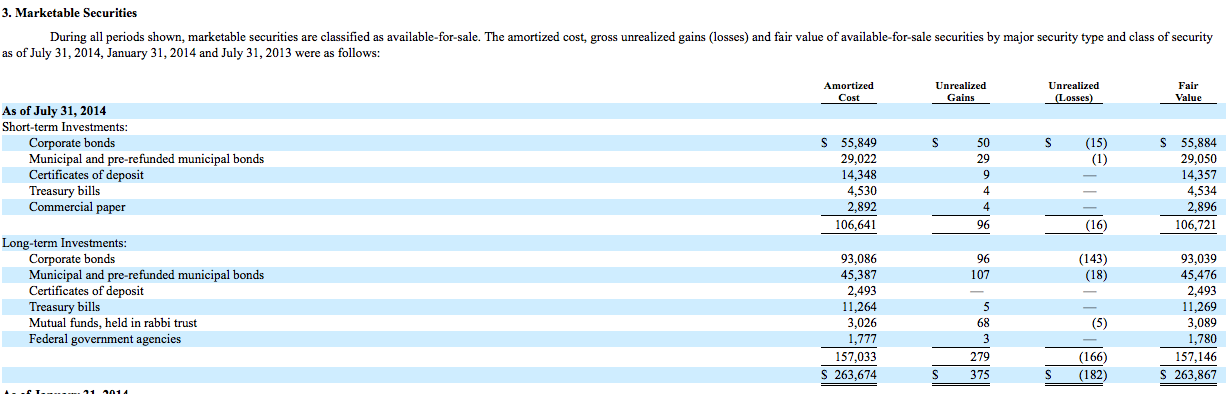

(click to enlarge)

Source: 10Q

It is important to notice that URBN has $157 million in marketable securities categorized as long-term investment on the balance sheet. In fact, when I calculate enterprise value of URBN, I utilize its current market cap of $4 billion minus the $409 million cash, cash equivalents and marketable securities in order to come up with $3.6 billion enterprise value, which I have already applied for in my valuation analysis section.

For the financial strengths of URBN, given the $409 million cash, cash equivalents and marketable securities, URBN has a lot of financial flexibilities with its pristine balance sheet.

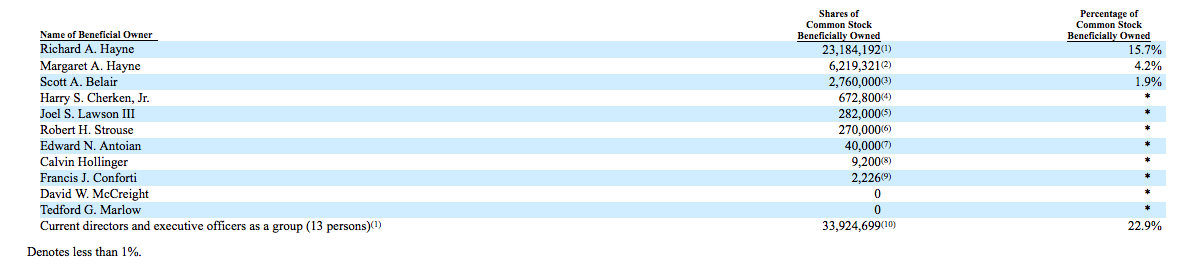

Management Team

(click to enlarge)

Source: Proxy Statement

Richard Hayne, as a founder, has in-depth knowledge about URBN. Plus, he has 28 years of experience in the retail industry. Hayne is the current CEO and the chairman of URBN, and owns 15.7% of the outstanding shares. In general, I like companies run by founders. I believe that since URBN is run by owner mindset, the economic interest of URBN should be more aligned with the minority shareholders.

In addition, directors and executive officers together own 22.9% of URBN. The ownership is significant and indicates that insiders have positive outlooks for URBN.

Risks

First, the highly promotional retail environment might last longer than anticipated. This can further drag the profit margins lower as retailers have to lower selling prices in order to clear up inventories. Plus, consumers might be accustomed to more and more promotions and wait for bargains. This might reduce the sales for full-priced products and further put pressure on profit margins. This trend might be more apparent for teenage-related retailers. Second, the fashion trend is very difficult to forecast, and the business nature of URBN is volatile. Third, with ample of cash on the balance sheet, there is possibility of URBN conducting dilutive acquisitions. However, based on historical track record of URBN, this risk seems to be low.

The Bottom Line

As we all know, the fundamentals of a company cannot change rapidly. However, stock price of any given company can move up or down more than 20% in a day. This sometimes gives a good entry price for patient investors to accumulate at a bargain price. I believe that such an opportunity has just arrived for URBN. With long-term investment horizon, URBN should be a good and solid investment in a well-balanced portfolio.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.