As WTI oil price continues to decline to the current $83, the signal of Saudis not to cut output further gives support for the downward momentum. However, the decrease in oil price can be a boom for heavy oil consumption companies, like Carnival (CCL, Financial). The immediate effect of oil price might not be apparent as the hedges in CCL will negate some benefits from the near-term oil prices. Nevertheless, if oil price continues to decline in the future, it can really help to lower the operating costs for CCL and eventually benefit the profit margins. Some might argue that the Ebola issue will negatively affect the travel sector. That's true. Nevertheless, for long-term investors, we should take advantage of short-term issues and accumulate stocks with good prospects and sound fundamental support. Looking forward, when CCL can turnaround the negative sentiments around recent accidents and have positive growths in net yields, CCL should be re-evaluated for 30% upside potential.

Company Overview

Carnival Corporation is a global cruise company and one of the largest vacation companies in the world. The portfolio of leading cruise brands includes Carnival Cruise Lines, Holland America Line, Princess Cruises and Seabourn in North America; P&O Cruises (UK), and Cunard in the United Kingdom; AIDA Cruises in Germany; Costa Cruises in Southern Europe; Iberocruceros in Spain; and P&O Cruises (Australia) in Australia.

Why did CCL decline?

The main reason Carnival gets relatively low expectation from the street is due to several accidents, such as the Costa Concordia accident in January 2012, and the Carnival Triumph fire which occured in February 2013. Without fundamental issue in the business and industry itself, the negative publicity and investment sentiment about CCL should only have a short term impact on Carnival's share price.

Another reason for the recent decline is due to the Ebola virus. The travel industry is unavoidably affected. And then there was the second case of Ebola in the U.S. But given the strong fundamental of CCL, I have no doubt that CCL will survive this short-term hiccup on the demand of traveling in the near future. Nevertheless, this does not alter my long-term view on CCL.

For prudent long-term investors in today's volatile stock market, it is good strategy to set up several limited orders to accumulate shares as the share price goes down. This strategy can help investors to average down instead of trying to time the rock bottom of CCL.

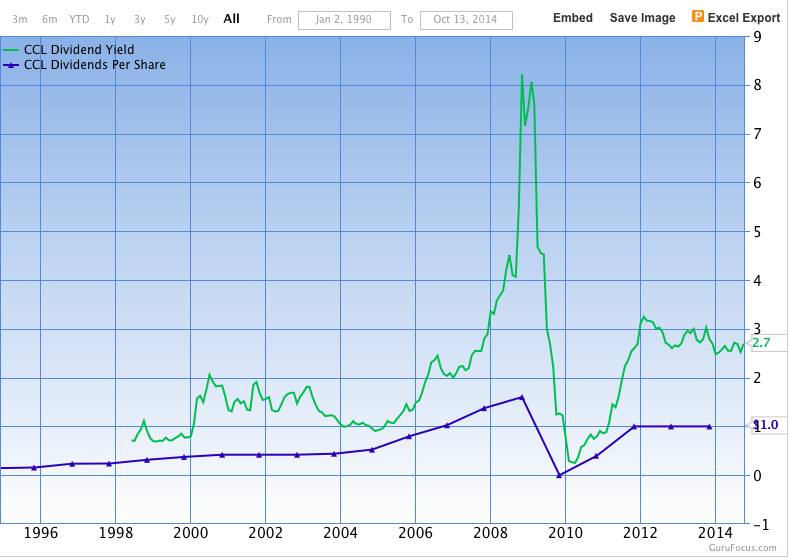

Valuation

(click to enlarge)

Source: Gurufocus.com

CCL has been able to find bottom close to 1x book value. As CCL is trading at $34.60, it is not far away from its book value of approximately $32.

(click to enlarge)

Source: Gurufocus.com

Other than the financial crisis period in 2009, CCL has shown its capability to increase dividends. Currently, CCL has 2.8% dividend yield. The high dividend yield helps to establish a stable shareholder base and provide support for the current share price.

Historically, Carnival has an average earning of $2.33 in the past 5 years. With today's price at $34.50, it is valuated at $2.26 EPS in 2015 with 15.5x PE. As CCL has 21.24% five year growth expectation, it will not be a stretch to value CCL at 20x P/E multiple. This results in my target price of $45 and implies 30% upside potential.

The Positive Outlook

First and foremost, most of cruising industry customers are the population with older ages. As one of the macro trend is aging population, CCL should be able to ride the aging population trend.

Furthermore, the expansion to other counties especially in Asia is tremendous. At present, there is less than $2 billion of total cruise industry revenues coming from Asia. As the middle class population increases in Asia, they tend to demand different types of traveling experiences, including cruising. The cruise industry is still practically non-existent in Asia. Why? Because Asians and Indians have some sort of cultural bias against cruising. Folks across the Pacific are equally sensitive (or more) to value and equally desirous (or more) of luxurious experiences. The infrastructure over there simply hasn't existed, nor have the incomes. But that's all starting to change in Carnival favor in the near future.

Management Team

(click to enlarge)

Source: Proxy Statement

Micky Arison used to be the CEO and the chairman of CCL. He retired from CCL after running the company for 34 years in June 2013. However, he still owns 23% stake in CCL. As he has already left CCL, his future selling of CCL can put pressure on the share price of CCL. This poses additional risk for prospective CCL investors.

Arnold W. Donald has been the CEO of CCL since 2013. He has industry expertise in the agriculture, biochemical, chemicals, and service sectors for over 30 years. More details about Arnold can be read on the Businessweek.com.

Risks

First, if there is any widespread disease, like Ebola, or a terrorist attack, the whole travel sector will be under pressure, including CCL. Second, fuel cost is an important driver for the profitability of CCL. As oil is forecasted to trend downward, I believe this will be the tailwind for CCL in the near future. Third, the brand image tarnishment might be more severe than anticipated by the accidents of CCL. If there will be any more future accidents in CCL, this might be viewed as the fundamental issues of CCL as the accidents seem to be recurring.

The Bottom Line

I believe that as CCL turnarounds and reverts back to more normalized earnings, the negative sentiments surrounding CCL will gradually dissipate. Plus, the positive underlying macro trend will eventually bring Carnival to a higher level. In the meantime, investors can collect 2.8% dividend yield while waiting the company for turnaround. I will recommend to buy Carnival at around $34 with 30% upside potential.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.