Source: Yahoo Finance

Titan International Inc. (NYSE:TWI) has been trading close to its 5 year low. In January of 2014, Barron's wrote a bullish article on TWI expecting a $21 target price. Since then, I have kept a keen eye on TWI. Today, as it declined by 7.6%, I revisited the buy thesis on TWI and see whether it is a good long-term investment. I found that after further deterioration in the macro wheel and tire industry TWI might not be able to reach $21 anytime soon. Nevertheless, I can see that TWI still has more than 40% upside potential. In my opinion, investors should give a second look at TWI and assess its intrinsic long term value.

Company description

TWI engages in the manufacture and sale of wheels, tires and undercarriage systems and components for off-highway vehicles used in the agricultural, earthmoving/construction and consumer markets in the United States and other countries. It has a dominant position in the farm wheel and tire business, controlling 75% of the North American off-the-road "OTR" market for farm wheels and 40% for tires. The leadership position in the North America off-the-road market for farm wheels and tires is the most important asset of TWI, and I believe that the well-established farm wheels and tires business is why some well-respected funds and activists got attracted to TWI. In addition, TWI has over 100 years of operational history as it was founded in 1890.

2014 management goals

The following is from TWI's press release:

The revenue goal for 2014 is set at $2.4 to $2.7 billion US dollars, assuming no further acquisitions. EBITDA goals are$240 million to $270 million. These figures presume pricing and material costs remain flat in 2014. In 2013, Titan saw pricing drop due to material decreases across all products. Titan forecasts maintenance Cap Ex to be approximately $70 million in 2014. All managers' bonuses will be based on reaching the above goals. Incentives are in place to improve the bottom line.

There are currently four acquisitions for which Titan is performing due diligence. If we complete these acquisitions, the maximum additional revenue would be approximately $500 million.

It was not long ago that TWI provided the mid-point guidance of $255 million EBITDA in 2014. This implied that TWI would trade at about 4.7x EV/EBITDA. Although the guidance has been lowerd since then, it is still worth to mention this and see the potential of TWI if the industry will turn around some day in the future.

The innovation of TWI

Another excerpt from TWI's press release:

We are excited about new opportunities that lie ahead for Titan in 2014. One of them is our new company, Titan Tire Reclamation Corporation, which operation will use a licensed pyrolysis system to reduce rubber tires to oil, steel and carbon black. A single 63" tire will convert into more than 500 gallons of oil and generate carbon credits. The recovered oil, carbon black and steel can be recycled into bio-diesel fuel; carbon black into green rubber products and steel into mining components such as bucket teeth. This business is a perfect fit for Titan Mining Services. We expect that many mining companies and contractors in the Canadian oil sands will sign up with TTRC next year due to the importance of recycling tires. After we are up and running with TTRC in Canada, Titan will open up locations in Chile and Australia where there are large amounts of used 63" tires to be recycled. I've just returned from the oil sands (it was -17â° F) and the amount of business up there is truly amazing. We are enthusiastic about the profit opportunities and process of going green.

"We have posted several Titan youtube videos of our LSW tire performance in the field. Titan's LSW tires are shown going head to head with CNH Quadtrac and Deere's track tractor. LSW tires beat the track tires and the fuel savings was an added benefit to the farmers. Tractors were able to save approximately 3-5 gallons per hour with the LSW tires. As a farmer would say, hard work and patience will pay off. We encourage our shareholders to view these videos to illustrate one of Titan's innovative concepts.

Paul G. Reitz, the CFO of TWI, summed up the innovation well and said that

Nobody can move as fast as we can, with the advantages we have with the wheel and the tire. But it isn't a short-term thing. It's a mid- to long-term enhancement, improvement and competitive advantage that we have.

I still believe that TWI has done a lot in regards to its businesses but the macro environment makes TWI have difficulty in making good amount of money in the meantime.

What caused TWI's recent decline?

The demand for big tires has slowed, and key customers had to upload many nearly new tires onto the market. From the macro point of view as written by Barron's below:

With expectations high for a large corn crop this fall, corn prices have tumbled mightily. They are off more than 30% in the past year. That's weighed on farmers' spending budgets for new equipment, and hurt business for Titan International, a maker of tires and wheels for farm, construction, and mining equipment.

The farmers, the key customers of TWI, are in financial constraint to upgrade or spend more money on tires. Furthermore, the rubber price declined in excess of 20% since the beginning of the year. As some tires are forced to sell close to the current depressed rubber price, the margins of TWI get further pressured to the downside.

Another reason for the decline in sales of TWI can be due to the weakness in cranes. As I followed Terex (NYSE:TEX), the sales of cranes are definitely in a downtrend, so too do the sales of the tires attached to the cranes.

What's more, corn, wheat and soybean prices have all declined close to 20% this year. This gives much less spending budgets for farmers. Plus, the mining industry is in a severe down cycle too. The combination makes the tires, sold together with the agricultural and mining machines, under significant pressure.

However, with long-term perspective, TWI definitely has the financial strengths to survive the still-challenging business condition in 2014. I will discuss more about the debts profile of TWI later in this article.

Valuation

(click to enlarge)

Source: Gurufocus.com

For the past decade, other than 2009, TWI has not traded close to 1x P/B ratio. As TWI has $12.7 per share book value, the market seems to undervalue TWI at the moment.

Based on the data of gurufocus.com, TWI had EBITDA of $166 million in 2011, $274 million in 2012, and $182 million in 2013. If we average the past three years' EBITDA, it will be $207 million. If we can hold a longer term investment horizon, I believe that TWI can eventually normalize its EBITDA to be close to $207 million in the future. With 6x EV/EBITDA, the enterprise value of TWI can be approximately $1.2 billion, which implies in excess of 40% upside potential.

(click to enlarge)

Source: Gurufocus.com

From the P/S ratio perspective, TWI currently trades close to 0.3x. For the past decade, TWI has not been trading close to this kind of level except during the financial crisis in 2009. As my pendulum analysis written on Datalink (NASDAQ:DTLK), I believe that the pendulum has swung too far into the pessimistic side, which provides a good entry point for prospective long-term investors in TWI.

Catalysts

TWI has a relatively small mining-tire operation business. If it is spun off or sought, it will help TWI to be more focused on its core business. Currently, the mining tires provide a high-margin-annuity-like revenue stream to TWI since mining tires typically wear out after nine months and mining trucks generally do not come with tires installed at the factory level.

In addition, activist MHR Fund Management acquired a 14% stake in June 2014, and Mark Rachesky got a board seat to help enhance shareholder value. The involvement of activists should give urgency to the management team to revive the business of TWI sooner rather than later.

TWI has done several acquisitions in the past and had experience in integrating businesses. As the wheel and tire industry going through a downtrend, TWI might do bolt on acquisitions in the near future. With a long-term investment horizon, I believe that the upcoming bolt on acquisitions should be accretive to the future earnings of TWI.

TWI also implemented a self-help cost savings program. It is expected to save around $15 to $17 million per year. In the latest quarter, TWI has already reduced headcounts by 800 workers. As the business outlook weakens, TWI has chosen to focus on what it can control, which is cost savings. Once the business environment improves, TWI will be in a better position to ride the cyclical uptrend.

The interest savings going forward

TWI redeemed its 7.875% senior secured notes due October 2017 by issuing new notes with an imputed interest rate of 6.277%. The following from the earning release states that the annual interest savings is about $0.13 per share.

So our annual interest savings going forward, as we look to next year, will be about $0.13 per share. Then looking at our debt structure after this transaction, we'll be at about $600 million of debt compared to at the end of the first quarter when we were at $865 million. So we really find ourselves with a simple structure of just those $400 million now outstanding in 2021 bonds, $60 million in outstanding converts and then another $130 million that will be overseas debt primarily located in Europe.

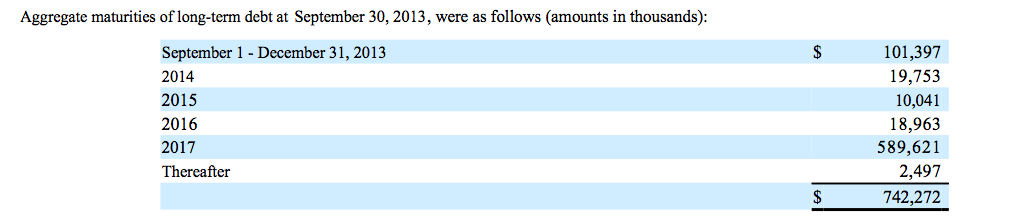

No long-term debt due

As shown in the 10Q below, the majority of long-term debt will not be due until 2017

(click to enlarge)

Source: 10Q

For a highly cyclical business like TWI, we have to check the debts profile to see whether TWI has enough capital to go through today's challenging period. As shown in the 10Q, the majority of TWI will be due in 2017, which should give TWI time to ride out today's tough environment.

Management team

(click to enlarge)

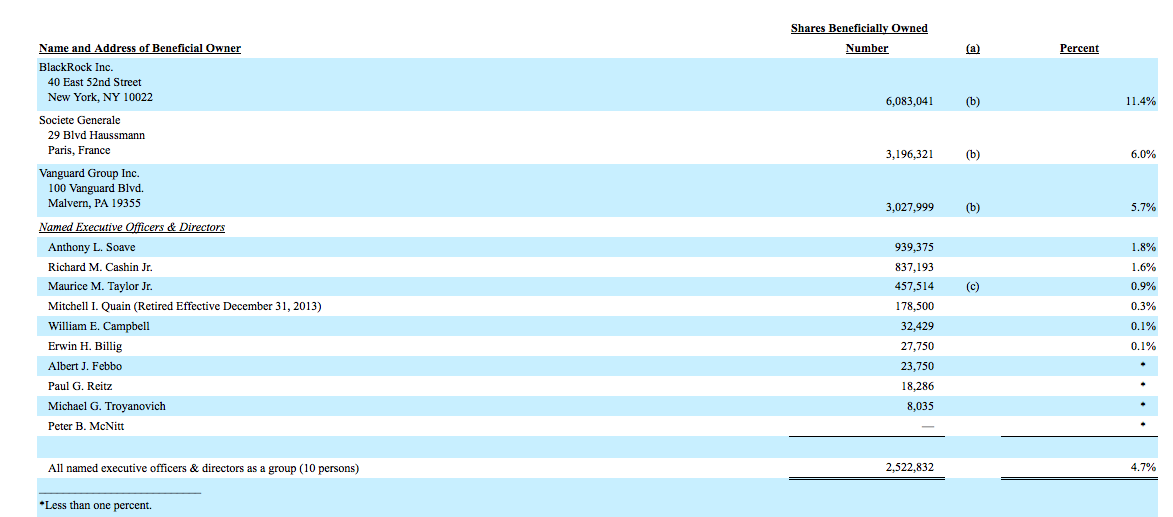

Source: Proxy Statement

According to the latest proxy statement, the executive officers and directors together owned 4.7% outstanding shares. Maurice Mannning, the CEO and the chairman of TWI, owned 0.9% outstanding shares. His ownership in TWI shows his confidence in the future of TWI. Maurice Manning has been with the wheel manufacturing business for over 30 years. Under Maurice's leadership, TWI has successfully acquired previously-failed businesses in the off-highway wheel and tire markets and become the Titan as of today. As I listened to the conference call held by Maurice Mannning, I could sense his vast knowledge in the wheel and tire businesses and his brunt style in directly communicating to his shareholders about what he has observed in the wheel and tire market.

John Hrudicka has been the CFO of TWI since February 3, 2014. His short tenure in TWI might be difficult for shareholders to see his contribution to TWI. However, he has been serving several industries, including Motorola, 3Com and Baxter Healthcare. I will strive to track his future performance as the CFO of TWI in the future.

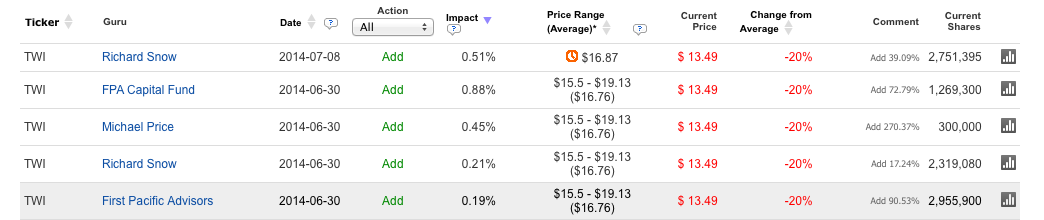

Guru trades

(click to enlarge)

Source: Gurufocus.com

Although there have been some buys and sells from Guru before June 2014, there have only been guru buys since June 2014. All details have been captured in the screen shot above.

Risks

First, TWI is subject to the volatility in crop prices. As crop prices drop, farmers will have less spending budgets to buy TWI tires. Second, TWI has customers concentration risk. Third, as tires demand is foreseen to be in decline in the near future, the decreasing sales volume might greatly impact the profit margins of TWI. However, I believe that TWI should have enough financial strengths to go through the current challenging business environment. Fourth, please refer to the risks section of the 10K to further understand the business risk investing in TWI.

The bottom line

TWI is not an investment for the faint of heart. TWI is volatile as it is in the cyclical business. The wheel and tire business might endure a longer down cycle than anticipated. However, for high-risk tolerant investors, the 40% upside potential is appealing. In addition, if the history of TWI is of any guide, TWI might not trade below its book value for long. Some investors might wait for the uptrend in the agricultural and mining industry before being bullish in the entire sector, including TWI. Nevertheless, if the uptrend comes, we have to ask ourselves whether TWI will still trade at today's bargained price. There is definitely risk involved in investing in TWI, but the 40% return should be enough to compensate for the risk.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.