Sometimes stocks screening cannot return the desired results. A good example is Bob Evans Farms (NASDAQ:BOBE). The reason is that the sum-of-the-part valuation with substantial real estate value embedded in the stock won't be revealed. In addition, the self-help margin expansion program won't be captured by stocks screening either. Furthermore, activist involvement will likely drive the management to show their capabilities managing the company. If the anticipated improvements are not realized, the activist will likely put more pressure on the management team or eventually break up the company for a sell at a premium valuation. Today, I would like to reveal what I find about BOBE and why BOBE deserves to trade at least 30% higher than its current share price.

Company overview

Bob Evans Farms composes of two key business segments: Bob Evans restaurants (72% of sales) and BEF Foods (28% of sales). Bob Evans restaurants operates 562 full-service restaurants located in 19 states with a heavy concentration in the Midwest. BEF foods produces and distributes refrigerated side dishes, pork sausage and a variety of refrigerated and frozen convenience food items through retail and food service channels.

(click to enlarge)

BOBE has the ambition to grow into a powerful national brands. Currently, BOBE has plans for transformation and growth. For BEF Foods, there will be side dish vertical integration, sausage network optimization from five facilities to two, and transportation consolidation. For Bob Evans Restaurants, the farm fresh refresh program will be completed in 2014, and BOBE plans to open 8 new restaurants in fiscal year of 2015.

BOBE has engaged in asset dispositions since 2006. It divested Mimi's cafe once realized the concept was not accretive to BOBE. Plus, BOBE closed 76 restaurants. This showed that BOBE would make tough strategic decisions to divest non-strategic businesses. I will pay close attention to see how the management team will work with the new board now with four seats advocated by Sandell Asset Management in the future.

(click to enlarge)

Source: Company Presentation

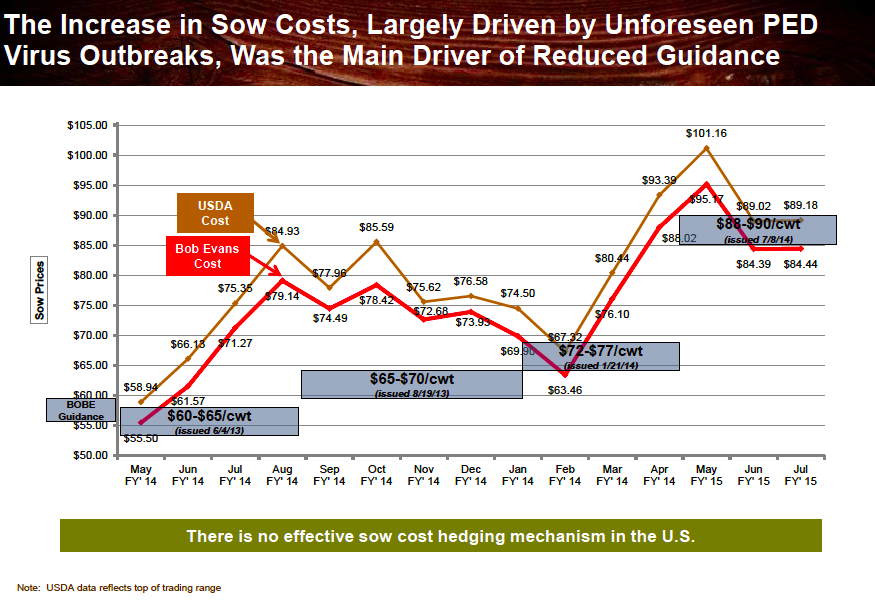

Despite the margin improvement efforts, it is worth noticing the rising trend of sow prices, a significant portion of costs. It has risen from around $55 to the peak of $95 as shown in the chart above. Since there is no effective sow cost hedging scheme provided in the U.S., prospective investors have to bear such price volatility risk by investing in BOBE.

Valuation

(click to enlarge)

Source: Company Presentation

BOBE demonstrated strong financial discipline. It doubled its dividend payments in 5 years. It has also decreased its outstanding shares by 27% since 2007. With its current market cap around $1 billion, BOBE has already returned over $625 million through stock repurchases since 2007 and further repurchased $225 million in 2014. It is a significant amount of capital the management team of BOBE already returned back to shareholders.

(click to enlarge)

Source: Company Presentation

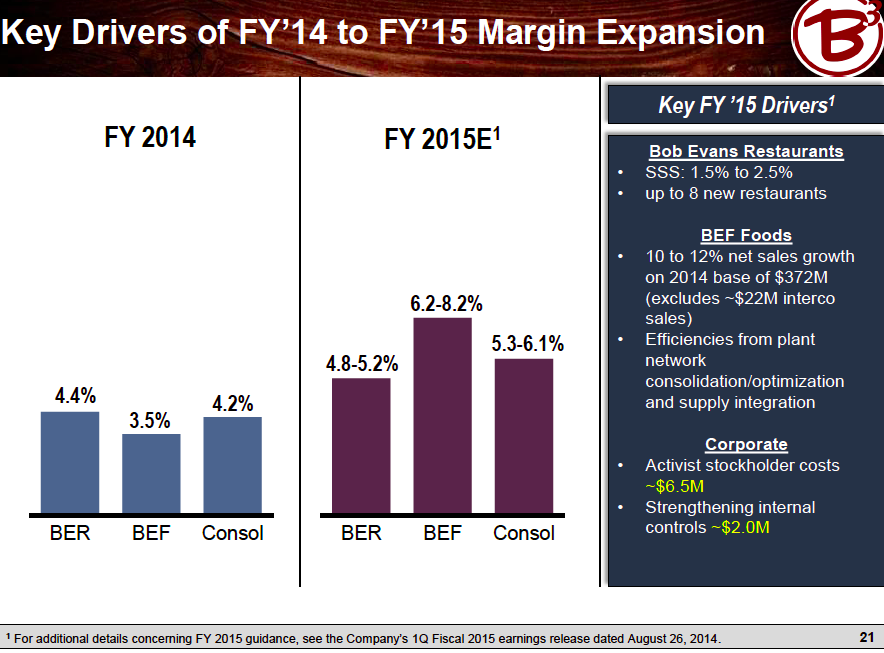

BOBE initiated margin expansion program. The most noticeable change is under BEF Foods. The management team of BOBE expected BEF Foods to grow the net sales by 10%-12% and increase its efficiencies from plant network consolidation and supply chain integration. It is forecasted to result in consolidated 5.3%-6.1% margins. Aside from the changes demanded by the activist involvement, BOBE has already had its own initiated expansion program to improve its margins. For instance, BOBE added a bakery and takeout section in each Bob Evans Restaurant to capitalize on the trend of carrying-out food.

Furthermore, BOBE has a new restaurant prototype, which can reduce building costs by approximately 13% through efficient design. What's more, BOBE is keen on innovating. It recently developed the compelling new Bob Evans Express license format. Although it is early to tell whether Bob Evans Express will be successful or not, prospective investors should be assured that BOBE is constantly improving and coming up with new idea to explore its farm heritage and expand to adjacent markets.

As Barron's reported below:

Management has so far rejected the recommendations, but if results don't improve, Sandell's calls for a breakup could become stronger.

In that scenario, too, shareholders could benefit. On a sum-of-the-parts basis, FrontFour's Gupta values the stock at $70 a share.

One way to benefit BOBE shareholders is through breakup. The other way is to implement good self-help programs to improve probabilities to reflect the true value of BOBE. As the sum-of-the-part valuation of BOBE can be $70 per share reported by Barron's, I am more conservative and expected BOBE to be worth approximately $58. We can think of the incremental values in two parts. First, if BEF Foods can be valued close to 13.4x EV/EBITDA, like the 35%premium valuation Tyson Foods (NYSE:TSN) paid to acquire Hillshire (NYSE:HSH), this will provide additional 15% upside potential. Another 15% upside potential can be realized through successful implementation of the margin expansion program. Given that there has already been activist involvement, I believe that my conservative 30% upside potential for BOBE to trade at $58 will be realized sooner rather than later.

Financial strengths

(click to enlarge)

Source: Company Presentation

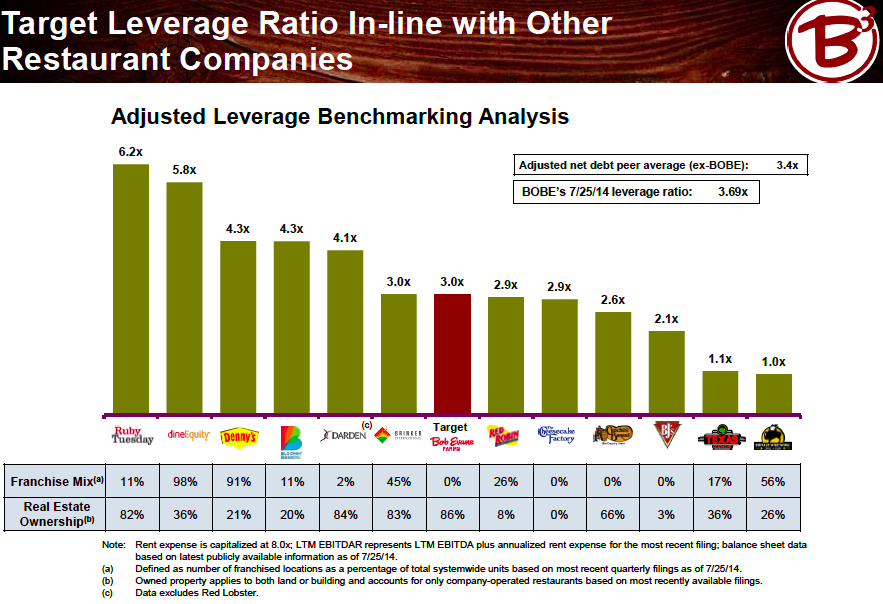

As BOBE has $462 million debts, It aimed to reduce its leverage ratio to 3x from 3.69x as of 7/25/2014. Currently BOBE has a slightly high leverage ratio compared to its peers. But once BOBE can achieve its 3x leverage ratio, it will be more in-line with its peers.

Even though BOBE has millions of debts on its balance sheet, BOBE has substantial real estate properties too.

ITEM 2. PROPERTIESThe following provides a brief summary of the location and general character of our principal plants and other physical properties as of April 25, 2014.

In March 2013, we sold our former corporate headquarters located at 3776 S. High St., Columbus, Ohio. We purchased approximately 41-acres of property in New Albany, Ohio, in December 2011 for the purpose of building a new corporate headquarters. The building and grounds were completed in October 2013.

We also own the Bob Evans Farm, a 937-acre farm located in Rio Grande, Ohio, and the Spring Creek Farm, a 30-acre farm located in Richardson, Texas. The Rio Grande, Ohio location supports our Bob Evans brand heritage and image through educational and tourist activities. The Richardson farm location is currently classified as held for sale, along with our Richardson, Texas, food production plant.

Bob Evans Restaurants Segment

At the end of fiscal 2014, we owned the real estate for 480 of our Bob Evans Restaurants and leased the real estate for the remaining 81 locations. The table located in Item 1 of this Annual Report on Form 10-K shows the location of all of our Bob Evans Restaurants in operation as of the end of fiscal 2014. The initial terms for the majority of our Bob Evans Restaurants' leases are 20 years and include options to extend the terms. Additionally, we own or lease properties for 20 closed restaurants and other storage facilities.

Source: 10K

As we can see from the 10K above, BOBE purchased 41 acres of property in New Albany, Ohio, to build a new corporate headquarter. BOBE also owned 937-acre farm located in Rio Grande, Ohio, and 30-acre farm located in Richardson, Texas. In addition, BOBE owned the real restate for 480 of Bob Evans Restaurants. As some estimated the real estate of BOBE worth about $900 million to $1 billion, but frankly I have no way to verify whether they are accurate or not. However, if BOBE sells some properties and leases them back to generate more capitals for future share repurchases, investors will soon have a better sense about the property values currently embedded in the balance sheet.

Management team

Steven Davis has been the CEO of BOBE since 2006. He served senior roles in several companies, including Long John's Silver restaurants, Yum! Brand (YUM), A&W restaurants, Marathon Petroleum Corporation (MPN, Financial), Walgreen Co. (WAG, Financial), Embarq Corp and Kraft (KRFT, Financial).

Currently, activist investor Thomas Sandell won four board seats out of 12 board seats. This will help to put pressure on the management team to perform. If not, activist is likely to put up more proxy fights and gain more control of the board.

Risks

First, BOBE is susceptible to the customer trend. If the gasoline prices increase and cause customers to drive less, there might be fewer customers who choose to dine in Bob Evans restaurants. This will result in fewer sales for BOBE. Second, BOBE depends on opening new restaurants to pursue its long-term growth strategies. There is execution risk. Plus, the restaurant business is highly competitive. Third, BOBE is subject to raw material costs for both its restaurant business and BEF Foods segment. In addition, the health care costs and rising minimum wages can also be sources of business operational risk for BOBE. Fourth, please refer to the risks section of the 10K to further understand the business risk investing in BOBE.

The bottom line

BOBE provides favorable risk/reward. The downside risks are likely limited by the real estate values, the margin improvement initiative carried by the current management, and the current 2.7% dividend yield. The upside potential can be 30% according to my estimation. As the recent acquistion of Hillshire illustrated, the BEF Foods, best-known for its sausages, should demand a premium if it will be sold as a separate company in the future. In addition to the self-help initiatives of BOBE to improve the Bob Evans Restaurant division, prospective investors should start to accumulate BOBE shares before the real value of BOBE is revealed.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.