Avista (AVA, Financial) has seen a daily gain of 1.82% and an Earnings Per Share (EPS) of 1.94. However, over the past three months, the stock has experienced a loss of 19.8%. The question arises: is the stock modestly undervalued? This article aims to answer this question through a comprehensive valuation analysis. We invite you to delve into the financial intricacies of Avista with us.

Company Introduction

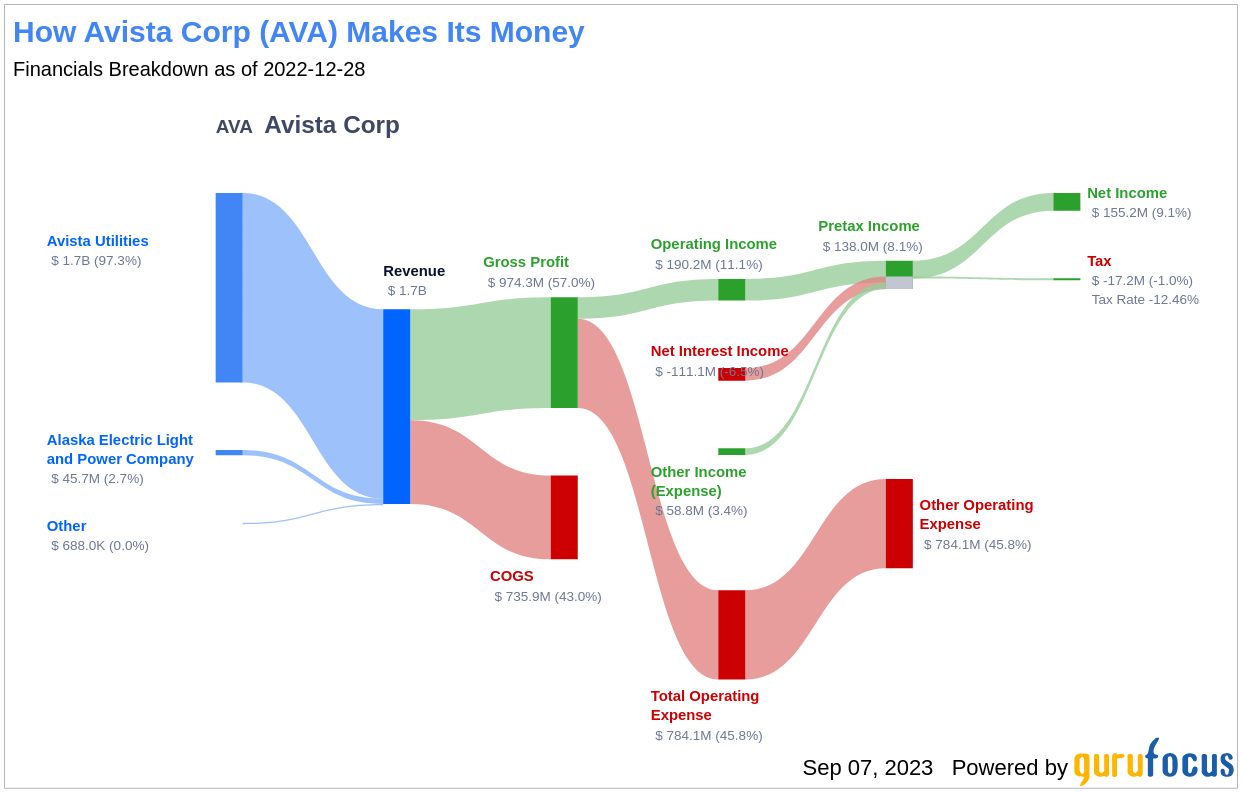

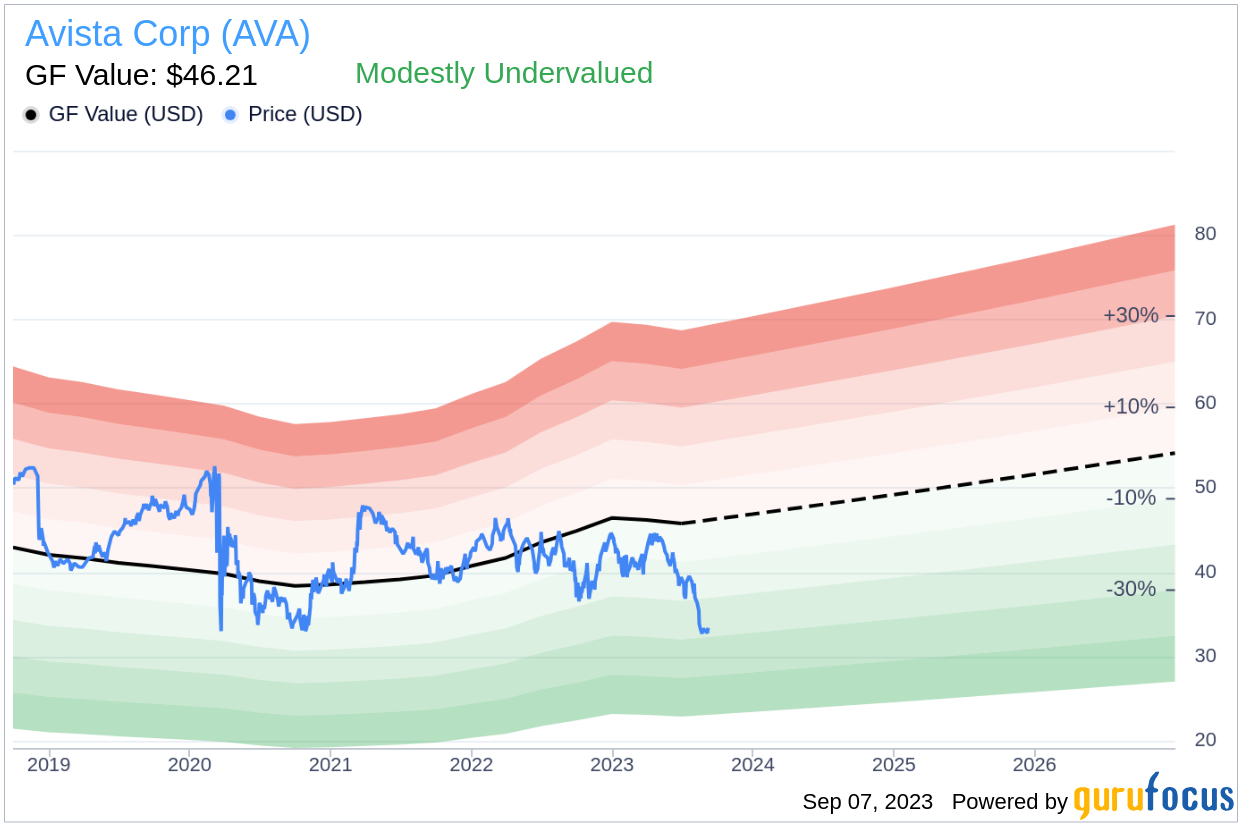

Avista Corp (AVA, Financial) is a well-established electric and natural gas utility company based in Spokane, Washington. The company primarily operates in the Pacific Northwest of the United States and in Juneau, Alaska. Avista's business segments include Avista Utilities, which provides electric distribution and transmission, and natural gas distribution services in parts of eastern Washington and northern Idaho. Avista Utilities also offers natural gas distribution service in parts of northeastern and southwestern Oregon. The current stock price is $33.52, while the estimated fair value, according to GuruFocus, stands at $46.21. This comparison suggests that Avista could be modestly undervalued.

GF Value: A Comprehensive Valuation Method

The GF Value is a proprietary valuation method that estimates a stock's intrinsic value based on historical multiples, an internal adjustment factor, and future business performance estimates. The GF Value Line on our summary page provides an overview of the fair value at which the stock should ideally trade. If the stock price is significantly above the GF Value Line, it is overvalued, and its future return is likely to be poor. Conversely, if it is significantly below the GF Value Line, its future return will likely be higher.

According to our GF Value estimation, Avista (AVA, Financial) appears to be modestly undervalued. This suggests that the long-term return of Avista's stock is likely to be higher than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength: A Closer Look

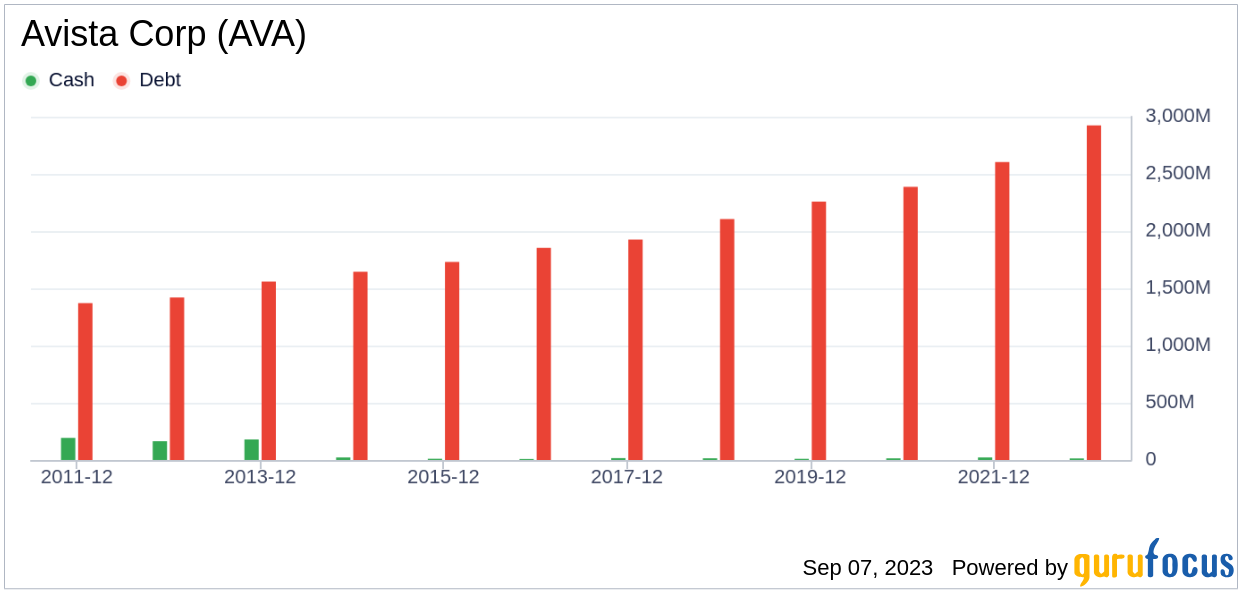

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it is crucial to carefully review a company's financial strength before deciding to buy shares. Avista has a cash-to-debt ratio of 0.01, which ranks worse than 95.2% of 479 companies in the Utilities - Regulated industry. Based on this, GuruFocus ranks Avista's financial strength as 3 out of 10, suggesting a poor balance sheet.

Profitability and Growth: A Key Factor for Valuation

Investing in profitable companies, especially those that have demonstrated consistent profitability over the long term, poses less risk. Avista has been profitable 10 over the past 10 years. Over the past twelve months, the company had a revenue of $1.70 billion and an Earnings Per Share (EPS) of $1.94. Its operating margin is 11.8%, which ranks worse than 51.41% of 496 companies in the Utilities - Regulated industry. Overall, GuruFocus ranks the profitability of Avista at 7 out of 10, which indicates fair profitability.

Growth is probably the most important factor in the valuation of a company. GuruFocus research has found that growth is closely correlated with the long-term performance of a company's stock. The faster a company is growing, the more likely it is to be creating value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth rate of Avista is 4.9%, which ranks worse than 65% of 480 companies in the Utilities - Regulated industry. The 3-year average EBITDA growth rate is -4.9%, which ranks worse than 77.9% of 457 companies in the Utilities - Regulated industry.

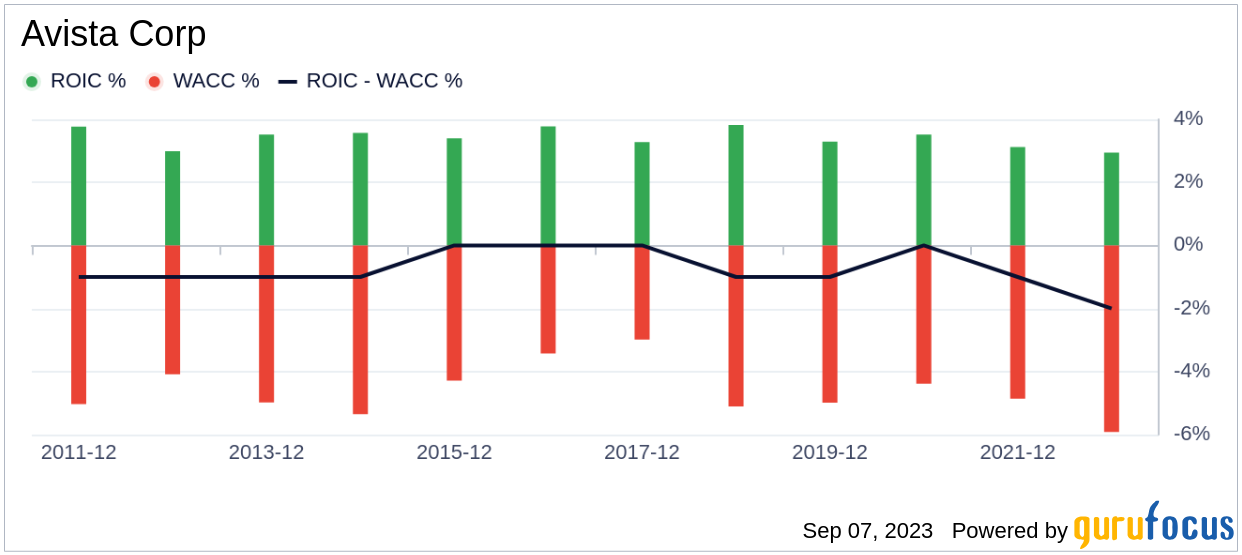

One can also evaluate a company's profitability by comparing its return on invested capital (ROIC) to its weighted average cost of capital (WACC). Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. If the return on invested capital exceeds the weighted average cost of capital, the company is likely creating value for its shareholders. During the past 12 months, Avista's ROIC is 3.24 while its WACC came in at 5.68.

Conclusion

In conclusion, the stock of Avista (AVA, Financial) appears to be modestly undervalued. The company's financial condition is poor, and its profitability is fair. Its growth ranks worse than 77.9% of 457 companies in the Utilities - Regulated industry. To learn more about Avista stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.