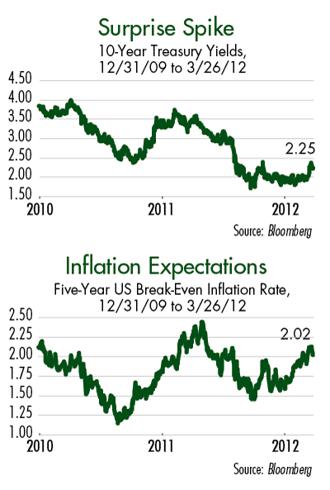

For much of the past nine months, U.S. 10-year Treasury yields have been range-bound between 1.8 percent and 2.1 percent, near record-low levels. The sudden spike in yields to around 2.4 percent in early March ranks among the most rapid moves in the Treasury bond market over the past decade and caught a lot of investors by surprise. (See “Surprise Spike.”)

The main catalyst for the jump in yields was a subtle change in the language of the Federal Reserve’s policy statement on March 13. The central bank altered its statement to predict moderate U.S. economic growth over the next few quarters, compared to the modest growth the Fed projected less than two months earlier in its late January policy statement.

The Fed also acknowledged improvement in global credit markets since the beginning of the year and a notable drop in the unemployment rate.

Some pundits immediately interpreted this statement to mean the Fed was rethinking its prior commitment to maintain exceptionally easy monetary conditions through at least late 2014. A handful of economists still predict that the Fed will begin hiking rates as soon as late 2012 or early 2013.

However, fears of a shift in the Fed’s monetary policy in 2012 or 2013 are misplaced. Likewise, fears about inflation and the future of U.S. monetary policy had little to do with the jump in yields.

The U.S. economic expansion since the end of the 2007-09 recession and financial crisis is not a normal recovery. U.S. households shouldered onerous levels of debt during the 2001-07 credit bubble and housing prices rose at a pace far above historic norms.

In prior post-war economic recoveries, consumers have helped push growth by ramping up spending and taking on credit. That hasn’t happened in this cycle, as consumers save more and shed debt.

Falling home prices and impaired mortgage debt are an additional headwind for the US economy. Home credit was a major driver of the boom in consumer spending through the middle of the last decade. Today, most consumers no longer have enough equity in their homes to obtain home equity lines of credit, which affords them less financial flexibility and makes them feel poorer.

Ever since the financial crisis eased in early 2009, I have espoused the view that the U.S. economic recovery would be anemic and unemployment would remain stubbornly high relative to prior economic expansions. History suggests that this is always true of economic recoveries in the wake of financial crises of the severity of 2007-09.

Of course, the economy rarely grows at a constant pace. There have been periods of slightly better growth and improving economic data such as over the past two quarters. However, two major recession scares have reared their heads since the last recession ended: the first in summer 2010 and the second, exacerbated by Europe’s financial crisis, in summer 2011. The underlying outlook for the economy hasn’t changed one bit.

Unwarranted Enthusiasm

Last summer, many investors assumed a modest deterioration in economic data was an early sign of impending recession; investors were far too pessimistic, offering a historic buying opportunity for stocks. As I’ve been writing over the past few issues of my advisory service, Personal Finance, some investors are now extrapolating more positive economic data this year as the beginnings of a boom. That outlook is way too optimistic; what we’re experiencing is a cyclical acceleration within the context of the same lackluster economic recovery.

Some of the recent improvement seems temporary. The fourth-warmest winter in modern U.S. history likely threw off the government’s seasonal adjustments to economic data, making job gains appear better than the underlying trend and boosting home sales and construction activity.

Over the next nine months, the U.S. economy faces several major hurdles, including a U.S. presidential election, still-fragile credit conditions in Europe, the looming expiration of tax cuts from the George W. Bush era, and major cuts to spending mandated as part of last summer’s debt ceiling compromise. I doubt all of the scheduled tax hikes and spending cuts will actually go into effect, but uncertainty is likely to persist until after the November election.

Fed chairman Ben Bernanke has made it clear that he’s well aware of the economy’s still-fragile state. Against that backdrop, the Fed is likely to err on the side of keeping interest rates too low for too long rather than threatening growth with a major shift in policy. Unless the data significantly improve over the summer, look for the Fed to retain its commitment to exceptionally low interest rates.

The five-year U.S. break-even inflation rate sheds light on the situation. (See “Inflation Expectations.”) To calculate this chart, I compared the yield on five-year U.S. government bonds to the yield on Treasury inflation-protected securities (TIPS). The yield on TIPS is adjusted for inflation each year; the market’s appetite for TIPs as compared to Treasuries indicates participants’ assessment of likely inflation trends.

The five-year break-even inflation rate continues to hover around 2%. While it has been rising since last summer when U.S. economic data began to improve, it’s still well below its 2011 highs. Unless inflation expectations begin to surge, the Fed will see little urgency to tighten policy.

A falling break-even inflation rate prompted the central bank to undertake a second round of quantitative easing in fall 2010. If break-even inflation begins to moderate again, the Fed may decide to launch a third round of quantitative easing. Over the next 12 months, I regard QE3 as a more likely outcome than an interest rate hike.

A more probable driver of the recent jump in Treasury yields is investors selling government bonds yielding less than 2% to buy riskier assets such as stocks and commodities. The risk-on trade that’s pushed stocks to their best first-quarter performance in over a decade is a negative for safe-haven investments such as U.S. government bonds.

As I stated in The Market is Still Vulnerable, investors have plenty of reasons to fear a stock market pullback, but the threat of tightening from the Fed isn’t one of them. The Fed also is bound to take into account the prospect of continued uncertainty in the oil market that has caused a spike in fuel prices.

Rising interest rates are generally a negative for income-producing stocks such as Linn Energy (LINE, Financial) and SeaDrill (SDRL, Financial). However, that’s unlikely to be the case this cycle because U.S. Treasury yields are still near record-low levels, even after the recent jump in yields.

Moreover, easing credit conditions in Europe and the global inter-bank lending markets over the past few months actually have pushed down borrowing costs for most large companies.

The main catalyst for the jump in yields was a subtle change in the language of the Federal Reserve’s policy statement on March 13. The central bank altered its statement to predict moderate U.S. economic growth over the next few quarters, compared to the modest growth the Fed projected less than two months earlier in its late January policy statement.

The Fed also acknowledged improvement in global credit markets since the beginning of the year and a notable drop in the unemployment rate.

Some pundits immediately interpreted this statement to mean the Fed was rethinking its prior commitment to maintain exceptionally easy monetary conditions through at least late 2014. A handful of economists still predict that the Fed will begin hiking rates as soon as late 2012 or early 2013.

However, fears of a shift in the Fed’s monetary policy in 2012 or 2013 are misplaced. Likewise, fears about inflation and the future of U.S. monetary policy had little to do with the jump in yields.

The U.S. economic expansion since the end of the 2007-09 recession and financial crisis is not a normal recovery. U.S. households shouldered onerous levels of debt during the 2001-07 credit bubble and housing prices rose at a pace far above historic norms.

In prior post-war economic recoveries, consumers have helped push growth by ramping up spending and taking on credit. That hasn’t happened in this cycle, as consumers save more and shed debt.

Falling home prices and impaired mortgage debt are an additional headwind for the US economy. Home credit was a major driver of the boom in consumer spending through the middle of the last decade. Today, most consumers no longer have enough equity in their homes to obtain home equity lines of credit, which affords them less financial flexibility and makes them feel poorer.

Ever since the financial crisis eased in early 2009, I have espoused the view that the U.S. economic recovery would be anemic and unemployment would remain stubbornly high relative to prior economic expansions. History suggests that this is always true of economic recoveries in the wake of financial crises of the severity of 2007-09.

Of course, the economy rarely grows at a constant pace. There have been periods of slightly better growth and improving economic data such as over the past two quarters. However, two major recession scares have reared their heads since the last recession ended: the first in summer 2010 and the second, exacerbated by Europe’s financial crisis, in summer 2011. The underlying outlook for the economy hasn’t changed one bit.

Unwarranted Enthusiasm

Last summer, many investors assumed a modest deterioration in economic data was an early sign of impending recession; investors were far too pessimistic, offering a historic buying opportunity for stocks. As I’ve been writing over the past few issues of my advisory service, Personal Finance, some investors are now extrapolating more positive economic data this year as the beginnings of a boom. That outlook is way too optimistic; what we’re experiencing is a cyclical acceleration within the context of the same lackluster economic recovery.

Some of the recent improvement seems temporary. The fourth-warmest winter in modern U.S. history likely threw off the government’s seasonal adjustments to economic data, making job gains appear better than the underlying trend and boosting home sales and construction activity.

Over the next nine months, the U.S. economy faces several major hurdles, including a U.S. presidential election, still-fragile credit conditions in Europe, the looming expiration of tax cuts from the George W. Bush era, and major cuts to spending mandated as part of last summer’s debt ceiling compromise. I doubt all of the scheduled tax hikes and spending cuts will actually go into effect, but uncertainty is likely to persist until after the November election.

Fed chairman Ben Bernanke has made it clear that he’s well aware of the economy’s still-fragile state. Against that backdrop, the Fed is likely to err on the side of keeping interest rates too low for too long rather than threatening growth with a major shift in policy. Unless the data significantly improve over the summer, look for the Fed to retain its commitment to exceptionally low interest rates.

The five-year U.S. break-even inflation rate sheds light on the situation. (See “Inflation Expectations.”) To calculate this chart, I compared the yield on five-year U.S. government bonds to the yield on Treasury inflation-protected securities (TIPS). The yield on TIPS is adjusted for inflation each year; the market’s appetite for TIPs as compared to Treasuries indicates participants’ assessment of likely inflation trends.

The five-year break-even inflation rate continues to hover around 2%. While it has been rising since last summer when U.S. economic data began to improve, it’s still well below its 2011 highs. Unless inflation expectations begin to surge, the Fed will see little urgency to tighten policy.

A falling break-even inflation rate prompted the central bank to undertake a second round of quantitative easing in fall 2010. If break-even inflation begins to moderate again, the Fed may decide to launch a third round of quantitative easing. Over the next 12 months, I regard QE3 as a more likely outcome than an interest rate hike.

A more probable driver of the recent jump in Treasury yields is investors selling government bonds yielding less than 2% to buy riskier assets such as stocks and commodities. The risk-on trade that’s pushed stocks to their best first-quarter performance in over a decade is a negative for safe-haven investments such as U.S. government bonds.

As I stated in The Market is Still Vulnerable, investors have plenty of reasons to fear a stock market pullback, but the threat of tightening from the Fed isn’t one of them. The Fed also is bound to take into account the prospect of continued uncertainty in the oil market that has caused a spike in fuel prices.

Rising interest rates are generally a negative for income-producing stocks such as Linn Energy (LINE, Financial) and SeaDrill (SDRL, Financial). However, that’s unlikely to be the case this cycle because U.S. Treasury yields are still near record-low levels, even after the recent jump in yields.

Moreover, easing credit conditions in Europe and the global inter-bank lending markets over the past few months actually have pushed down borrowing costs for most large companies.