Deswell Industries (DSWL, Financial) manufactures plastic, metal and electronic components for equipment manufacturers. As one might expect, business has slowed as a result of the recession. Revenues fell almost 40% in 2010, but they have started to tick back up in recent quarters. Meanwhile, the stock price has fallen some 75% since its 2007 high.

As a result, the company trades for just $55 million while it has a cash position of $33 million, zero debt and operating income of a combined $22 million in 2007 and 2008. In addition, the stock trades at a slight discount to the company's net current assets. Clearly, if earnings can return anywhere close to where they were before the recession, this investment should pay off handsomely.

Often, value investors can make money by investing in cyclical companies when things look bleak. But to be successful in doing so, they must be able to distinguish between situations that are temporary (i.e. cyclical) versus those that are permanent (i.e. secular). Deswell presents a challenge in this regard due to a key factor.

First, the company is located in China. Before you automatically close this window and return to stalking your cousin's friend on Facebook, consider that Deswell is not one of those newly arrived reverse-mergers that have put Chinese stocks in the doghouse. It has been around since 1993, and has been public in the US since 1995.

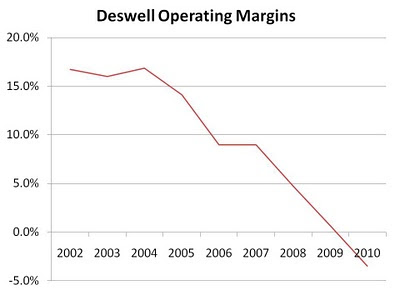

But while the company might be real, the fact that it's from China still presents a potential danger in this industry. China's high rate of inflation means the costs of labour are going up (an important cost for Deswell), but customers outside China don't seem willing to pay the higher costs. This has resulted in a consistently falling operating margin for the company, as shown below:

The chart above shows that the company was having difficulty passing on cost increases (either through competition, inflation, or both) even before the recession. More recently, China raised its minimum wage by over 20%, which was cited by Deswell as one of the reasons for the gross margin contraction in its most recent quarter. Further inflation could send customers to other low-cost countries.

Deswell appears cheap on both an assets and earnings perspective. However, it's unclear what component of its current earnings shortfall is cyclical vs secular, making it difficult to determine the company's earnings power. If the company can keep capital expenditures as low as it has recently, however, it may still be cheap on a free cash flow basis when combined with its strong financial position.

Disclosure: No position

As a result, the company trades for just $55 million while it has a cash position of $33 million, zero debt and operating income of a combined $22 million in 2007 and 2008. In addition, the stock trades at a slight discount to the company's net current assets. Clearly, if earnings can return anywhere close to where they were before the recession, this investment should pay off handsomely.

Often, value investors can make money by investing in cyclical companies when things look bleak. But to be successful in doing so, they must be able to distinguish between situations that are temporary (i.e. cyclical) versus those that are permanent (i.e. secular). Deswell presents a challenge in this regard due to a key factor.

First, the company is located in China. Before you automatically close this window and return to stalking your cousin's friend on Facebook, consider that Deswell is not one of those newly arrived reverse-mergers that have put Chinese stocks in the doghouse. It has been around since 1993, and has been public in the US since 1995.

But while the company might be real, the fact that it's from China still presents a potential danger in this industry. China's high rate of inflation means the costs of labour are going up (an important cost for Deswell), but customers outside China don't seem willing to pay the higher costs. This has resulted in a consistently falling operating margin for the company, as shown below:

The chart above shows that the company was having difficulty passing on cost increases (either through competition, inflation, or both) even before the recession. More recently, China raised its minimum wage by over 20%, which was cited by Deswell as one of the reasons for the gross margin contraction in its most recent quarter. Further inflation could send customers to other low-cost countries.

Deswell appears cheap on both an assets and earnings perspective. However, it's unclear what component of its current earnings shortfall is cyclical vs secular, making it difficult to determine the company's earnings power. If the company can keep capital expenditures as low as it has recently, however, it may still be cheap on a free cash flow basis when combined with its strong financial position.

Disclosure: No position